Answer:

Option (b) 15.0 percent

Explanation:

Data provided in the question:

Value of the bonds issued in Philippines pesos (PHP) at par = 500,000

Coupon rate = 15 percent

Now,

In the given question the bonds are issued at par.

Also, over the life of the bonds the exchange rate remains stable and until maturity the bonds are held

Therefore,

the financing cost will be equal to the coupon rate of the bond. i.e 15%

Hence,

Option (b) 15.0 percent

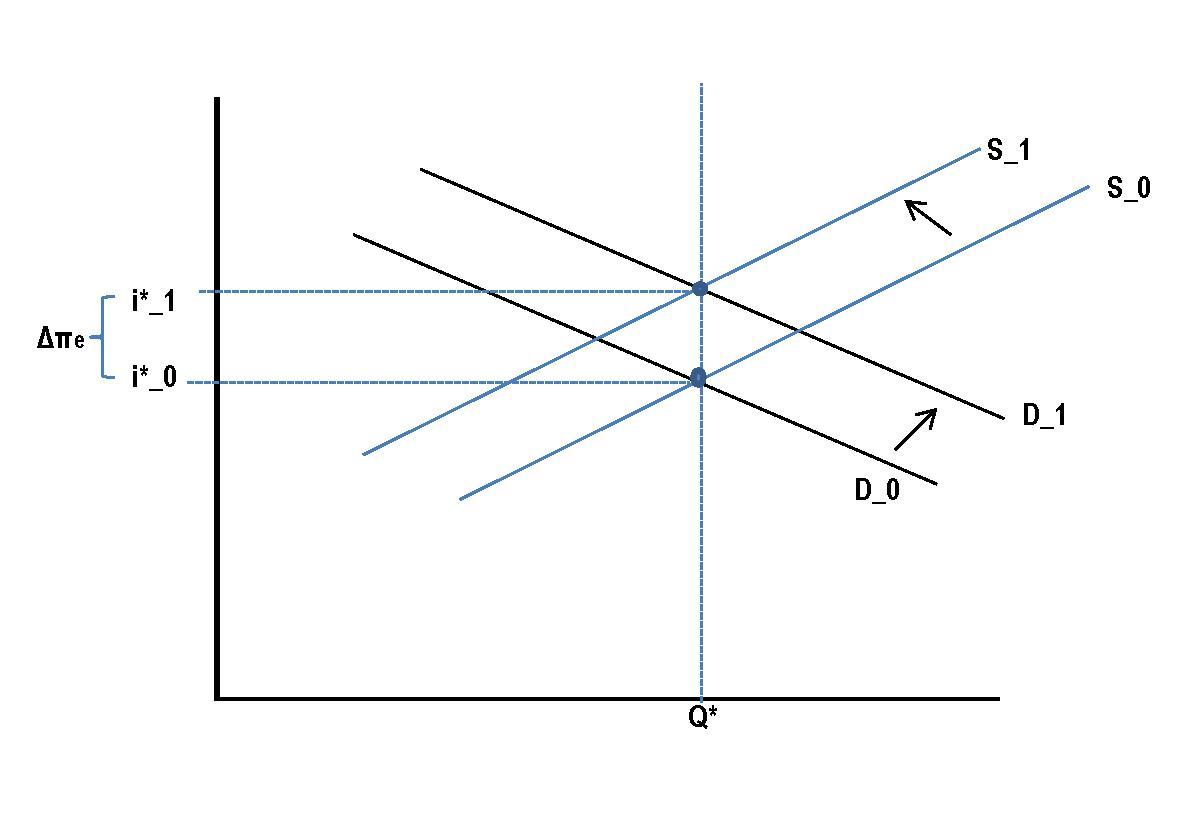

Answer:

shift demand and supply for loanable funds to the right (up), increasing interest rates.

Explanation:

According to the Fisher hypothesis when there is an increase in the expected inflation there is an equal increase in nominal interest rates.

As interest rates rise demand and supply for loanable funds will rise. This is illustrated in the attached diagram. Interest rate moves from i0 to i1.

Inflation is a reduction in the purchasing power of money. When inflation increases money regulation agencies reduce supply of money as a way to reduce price increase. This in turn reduces the amount of loanable funds commercial banks have to give out

To consider this question, we must consider the relationship between the resources and their costs.

Labor: The price that companies pay for labor is the wage. The businesses paid $68 billion for labor

Land: The price of land that business pay is rent (assuming they do not own the land). The business paid $14 billion for land.

Capital: The cost of using capital is the interest paid on that capital. The businesses paid $24 billion for using capital.

This leaves entrepreneurial ability. It is more difficult to discern the payment for this resource, as it is less tangible and thus has a less direct cost. From the payment for other resources and the total payment to households, we can infer the payment for entrepreneurial ability:

120 - 68 - 14 - 24 = $14 Billion

Answer:

Check the explanation

Explanation:

Using the percentage-of-completion method <em><u>(which is an accounting method or technique in which the earnings and expenses of contracts that are of long-term basis are documented as a percentage of the completed work during a particular period.)</u></em>

Total costs = Incurred costs + estimated costs to complete = $8 million + $12 million = $20 million

Revenue to recognize = $8m/$20m*$28m = $11.2 million

Gross Profit = Revenue recognized less costs incurred

= $11.2m - $8m = $3.2 million

Answer:

The journal entry for disposal of equipment will be as follows;

Explanation:

Accumulated Depreciation Dr.$98,000

Cash Dr.$40,000

Loss on disposal (150-98-40) Dr.$12,000

Equipment Cr.$150,000