Answer:

Depreciation for year 3 = $115518

BV = $57798

Explanation:

The modified accelerated cost recovery method employees a classification-based approach to depreciating certain assets, once classified are assigned respective rates of depreciation. for example, assets classified under automobiles, trucks and machinery are treated under 5-year MACRS and will be depreciated at 20%, 32%, 19.2% and so on.

In this question the bridge across Rio Grande being built by Del Norte Brick co is treated under 3-year MACRS, for which the rates are as follows:

33.33% for the first year

44.45% 2nd year

14.81% 3rd year

7.41% 4th year

We have been asked to determine 3rd years' depreciation and book value, determined as follows:

Depreciation year 1: $780000 33.33% = $259974

Depreciation year 2: $780000 44.45% = $346710

Depreciation year 3: $780000 14.81% = $115518

So the depreciation for year 3 = $115518

The book value is calculated as follows:

<em>Book value = cost - accumulated depreciation</em>

BV = $780000 - $722202

BV = $57798

Answer: $37.5 million

Explanation:

The next year's net income for XYZ will be calculated as follows:

Current sales = $300 million

Current Profit margin = 10%

Sales Growth rate = 25%

The next year's sales will be:

= Current Year's Sales × (1 + Sales Growth rate)

= $300 million × (1 + 0.25)

= $300 million × 1.25

= $375 million

Next Year's Net Income will then be:

= $375 million × 10%

= $37.5 million

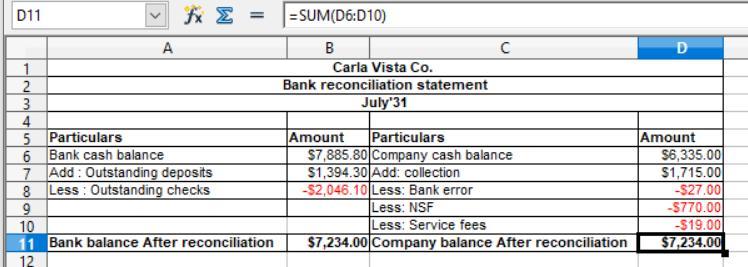

Explanation:

The preparation of the bank reconciliation statement is presented below in the attachment.

As we know that

The Bank reconciliation works with the balance of the bank statement and the balance of the cash statement. The aim is to compare those two statements to allow the organisation to operate smoothly.

There are various transactions because of which the balance of the bank statement and the balance of the cash statement do not match. We change the transactions correctly to match those statements.

The bank error is

= $374 - $347

= $27