Mobile marketing has a unique ability to empower users by connecting with them individually and continuously. This socially networked world will lead to connected users having more direct interactions with sellers.

What is marketing?

Creating interest in your company's goods or services is known as marketing. This is accomplished by market research, analysis, and comprehension of the interests of your prospective clientele. Product creation, distribution channels, sales, and advertising are all included in the definition of marketing.

What is the importance of marketing?

The benefit of marketing for your company is that it engages consumers and helps them decide whether to purchase your goods or services. Additionally, your business plan's marketing strategy contributes to the creation and maintenance of demand, relevance, reputation, competition, etc.

What is Direct digital marketing?

Delivering pertinent messaging electronically to chosen recipients is known as direct digital marketing (DDM). In the same manner that direct marketing in the real world uses the postal service, DDM uses email, websites, and mobile services.

Learn more about marketing: brainly.com/question/14083500

#SPJ4

30% Percentage of a person's effectiveness in a leadership role is due to heredity.

A leader can play various roles, and a firm will benefit more if they do so. Employees will be motivated to perform better, complete their goals, and even acquire leadership skills when they observe effective leaders in action.

Obtaining cooperation at the highest level is crucial for the creation of plans and policies. It is necessary for the interpretation and execution of plans and programs created by the top management at the medium and lower level. When plans are being carried out, leadership can be demonstrated by advising and guiding subordinates.

To know more about leadership, click here:-

brainly.com/question/14569585

#SPJ4

B - they must minimise the threats

Answer:

Cost to retail ratio = 57.05%

Explanation:

Particulars Cost Retail

Beginning Inventory $46,000 $66,000

Add: Purchases $213,000 $406,000

Less: Purchases Return $7,000 $9,000

Freight In $15,558 -

Net Markups - $6,400

Good Avail. for Sales (Without markdowns) $267,558 $469,000

Cost to retail ratio = $267,558/$469,000

Cost to retail ratio = 0.570486

Cost to retail ratio = 57.05%

Answer:

Note: <em>The organized question is attached as picture</em>

<em />

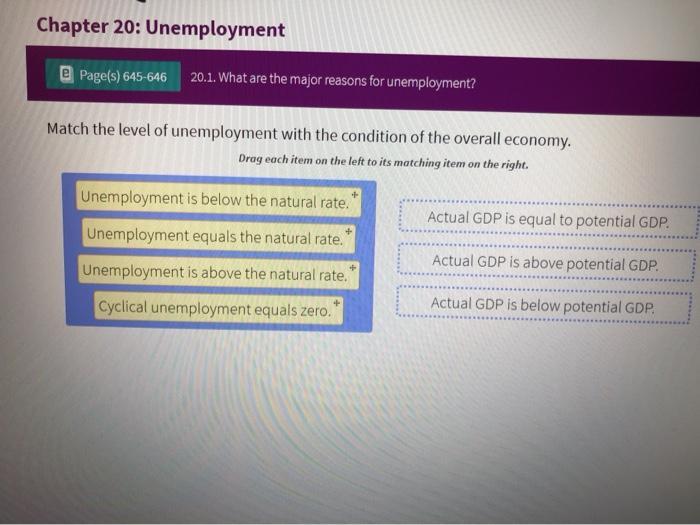

1. Actual GDP is below potential GDP

Level of unemployment: Unemployment is above the natural rate

2. Actual GDP is equal to potential GDP

Level of unemployment: Unemployment equals the natural rate

3. Actual GDP is above potential GDP

Level of unemployment: Unemployment is below the natural rate