Answer:

Increase.

Explanation:

The question above refers to auto insurance premium, which is a system that, through a monthly payment, allows an insurer to provide financial support to car owners as a form of security in case of accidents or injuries during driving. .

Many people do not know, however, under contracts with car insurers, smaller deductibles cause the premium to increase, making the individual responsible for insurance need to pay a higher monthly amount. A higher deductible, on the other hand, would reduce the value of the premium. In this case, we can say that if Deon chooses a lower deductible, he will have the high premium.

Answer:E. POLICYMAKERS WILL TAKE ACTIONS THAT ARE LIKELY TO RESULT IN THEIR BEING RE-ELECTED

Explanation: Public choice model suggests that public officials like political office holders will most likely use ECONOMIC POLICIES to ensure they achieve a personal desire or desires such RE-ELECTION.

Public office holders have come to realize that Voters choice are influenced by Government policies,they always want to implement policies that will influence the choice of voters.

Answer and Explanation:

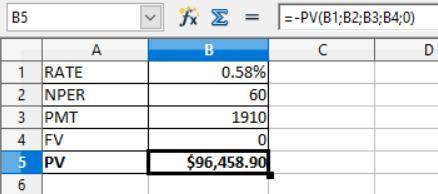

The computation is shown below:

First we have to find the present value based on monthly payment i.e. to be determined by using the present value formula and the same is to be shown in the attachment

Given that,

Future value = $0

Rate of interest = 7% ÷ 12 months = 0.58333%

NPER = 5 years × 12 months = 60 months

PMT = $1,910

The formula is shown below:

= -PV(Rate;NPER;PMT;FV;type)

So, after applying the above formula, the present value is $96,458.90

As it can be seen than the lumpsum amount i.e. $92,000 is less than the monthly payment present value so here the lumpsum option should be chosen.

Answer:

$5,000

Explanation:

The computation of total amount of excess fair over book value amortization expense adjustments to be recognized by red is shown below:-

Excess of fair value over book value = Land fair value - Land book value

= $52,000 -$42,000

= -$10,000

Here land is not amortized

Excess of fair value over book value = Building fair value - Building book value

= $390,000 - $200,000

= $190,000

Excess fair value over book value amortization expense adjustments to be recognized by red = Excess of fair value over book value of building ÷ Number of Years

= $190,000 ÷ 10

= $19,000

Excess of fair value over book value = Equipment fair value - Equipment book value

= $280,000 - $350,000

= ($70,000)

Excess fair value over book value amortization expense adjustments to be recognized by red for equipment = Excess of fair value over book value of equipment ÷ Number of Years

= ($70,000) ÷ 5

= ($14,000)

Total amount of excess fair over book value amortization expense adjustments to be recognized by red

= $19,000 - $14,000

= $5,000

Answer

x and y axis representing

Explanation: