Answer:

$6,500 was distributed to preferred shareholders

Explanation:

Dividend distributed to preferred share is based on the predetermined rate associated with these share. When the dividend is declared preferred share dividend is paid first. The remainder is distributed between the common stockholders.

Value of Preferred share = 8000 shares x $10 par value = $80,000

Preferred Dividend = $80,000 x 5% = $4,000

Accrued dividend of 2016 = $4,000 - $1500 = $2500

Total Dividend Accrued = $2,500 + $4,000 = $6,500

<span>Tina's mother and father pay her car insurance as long as she makes good grades. This is an example of which economic concept? Positive incentive. A positive incentive is a value that is given during the performance of a regular behavior. As long as Tina does what she is supposed to her parent's will continue to pay her car insurance. There is a reward for her doing what she </span>should be doing on her own which is motivating her to continue to do it.

Answer:

Marginal cost, average variable cost, and average total cost will increase. Average fixed cost will not change.

Explanation:

Marginal Cost is the change in total cost as a result of producing one extra unit of output.

Variable cost is cost that varies with output level. Average variable cost = variable cost / quantity produced

Fixed cost is cost that doesn't vary with the level of output produced. Average fixed cost = Fixed cost / quantity produced.

Total cost is the sum of fixed and variable cost. average total cost is total cost / quantity produced.

If the price of supplies increase, the cost of production increases and average total cost, average variable cost and marginal cost would increase.

Fixed cost would remain the same.

I hope my answer helps you

Answer:

As the actual price of such bonds should be $950.51 and the bonds are offered at a lower price, the bonds should be bought at the offered price.

Explanation:

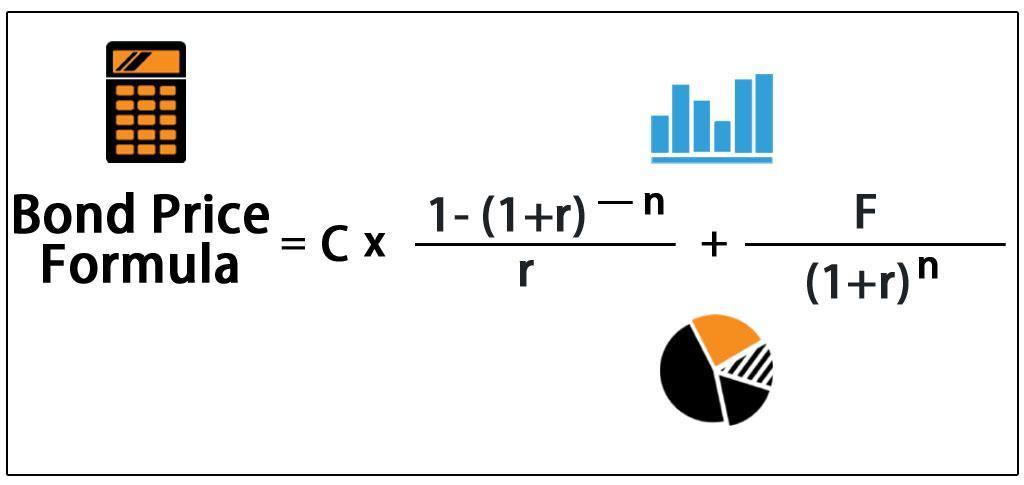

To determine whether the bonds should be bought at the given price or not, we first need to calculate the price of the bond. The formula for the price of the bond is attached.

The interest payed by the bonds can be treated as an annuity.

The semiannual rate will be = 9% / 2 = 4.5%

The number of semi annual payments will be = 7 * 2 = 14

The YTM expressed semi annually will be (r) = 10% / 2 = 5%

Semi annual coupon payment or C = 1000 * 0.045 = 45

Bond Price = 45 * [(1 - (1+0.05)^-14) / 0.05] + 1000 / (1+0.05)^14

Bond Price = 950.5068 rounded off to $950.51

As the actual price of such bonds should be $950.51 and they are offered at a lower price, the bonds should be bought at the offered price.