Answer:

A. 6.75%

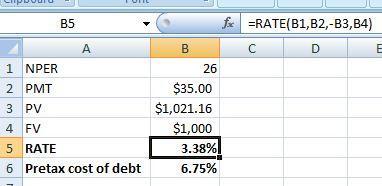

Explanation:

In this question, we use the Rate formula which is shown in the spreadsheet.

The NPER represents the time period.

Given that,

Present value = $1,021.16

Future value or Face value = $1,000

PMT = 1,000 × 7% ÷ 2 = $35

NPER = 13 years × 2 = 26 years

The formula is shown below:

= Rate(NPER,PMT,-PV,FV,type)

The present value come in negative

So, after solving this, the pretax cost of debt is 6.75% (3.38% × 2)