Answer:

Bad debt expense 6,500 debit

Allowance for uncollectible account 6,500 credit

Explanation:

"determined that there should be an allowance for uncollectible accounts of $5,150 at December 31, 2022."

We need to recognize as much bad debt as it need to leave the allowance balance on our expected uncollectible account.

balance for allowance before adjsutment:

beginning - write-off = unadjusted allowance

1,250 - 2,600 = -1,350

expected balance - unadjusted balance = adjustment

5,150 - (-1,350) = 6,500

Bad debt expense 6,500 debit

Allowance for uncollectible account 6,500 credit

Answer:

$406,000

Explanation:

Calculation to determine the actual total direct labor cost for the current period

Using this formula

Actual direct labor cost=Standard direct labor cost + unfavorable rate variance - favorable efficiency variance

Let plug in the formula

Actual direct labor cost=$400,000 + $10,000 - $4,000

Actual direct labor cost= $406,000

Therefore the actual total direct labor cost for the current period is $406,000

Answer:

Cost of goods sold =$61,5300

Gross Profit = $144,700

Explanation:

Given the information:

- Purchase : $630,000

- Purchase Returns and Allowances $25,700

- Prchases Discounts $10,900

- Freight-In $18,300

- beginning inventory of $45,000

- ending inventory of $64,600

- net sales of $760,000

As we the, the fomular for total Goods Available for Sale

=

Beginning Inventory + Purchases + Freight-In - Purchase Returns and Allowances - Purchases Discounts

= $45,000 + $630,000 + $18,300 - $25,700 - $10,900

= $67,9900

=> Cost of goods sold = Total Goods Available for Sale - ending inventory

= $67,9900 - $64,600

= $61,5300

=> Gross Profit = Net sales - Cost of goods sold

= $760,000 - $61,5300

= $144,700

Hope it will find you well.

Answer:

answer can be seen in the attached file

Explanation:

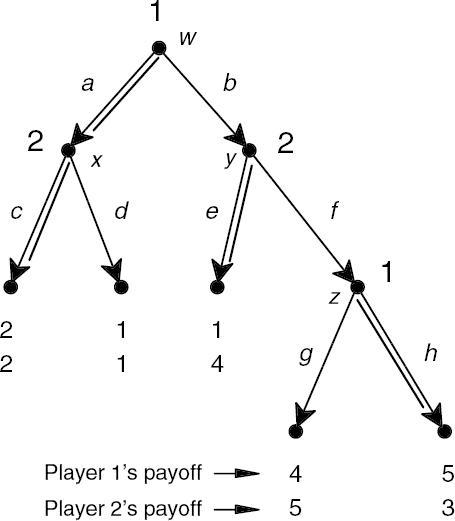

Consider the game in extensive form above. In the backward induction solution to this game Player 1 plays strategy and Player 2 plays strategy (Please, label Player 1's strategies by A, B, and C, and Player 2's strategies as df, dg, ef, and so forth)

What is Game Theory?

This is a mathematical modelling that deals with the analysis of strategies for dealing with competitive situations where the result of a participant's choice of action depends critically on the actions of other participants. Game theory has been applied to in war, business, and biology, sport.

In Game theory, outcome is dependent on the contributions of competing parties

The student loan debt has the highest consumer debt balance.

Below is an explanation about student loan debt.

<h3>What is Student Loan debt</h3>

Student debt is a type of debt that is owed by a current student, a formerly withdrawn student or graduated student to a lending institution, or to a financial institution

This type of loan has the highest consumer debt balance.

Lean more about types of debt at brainly.com/question/2754850