Answer:

hello your question lacks the required file ( excel file ) attached below is the missing file

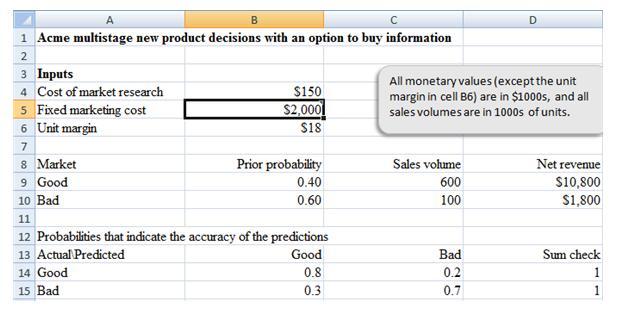

Answer : The EVI does not change in the way expected and this is because of the higher probability assignment

Explanation:

1) calculate the EVI for the first combination

i.e. B5 = $2000, B9 = 0.4, B14 = 0.8, B15 = 0.3

EVI = EMI with information - EMI without information

= 3250 - 3400

= $ 150

<em>note : EMI with information is gotten via solution tree </em>

2) Calculate the EVI for the second combination

i.e. B5 = $4000 , B9 = 0.3 , B14 = 0.9, B15 = 0.2

EVI = EMI with information - EMI without information

= $1378 - $500 = $878

Well, based on the problem, it seems that after that one year of having a large volume of sales, you probably became complacent and noticed that you have less orders. So I would say that you probably failed to continue your marketing efforts. it is very important for a company to always continue their marketing efforts because it is through the marketing efforts that they will be able to bring in sales. if you stop your marketing efforts even for a bit, you will see that there is a decline in sales.

Answer: $0 billion

Explanation:

Money spent for consumption is the difference between Disposable income and Savings.

Disposable income increase:

= 1,092 - 912

= $180 billion

Savings increased by $180 billion which is equal to the change in Disposable income.

Change in consumption = Change in disposable income - change in savings

= 180 - 180

= $0 billion

Explanation:

While there are literally dozens of soft skills that comprise a great manager, communication, leadership, delegation and trustworthiness are some of the most important qualities.

Communication. ...

Leadership. ...

Listening. ...

Delegation. ...

Critical Thinking. ...

Trustworthiness. ...

Networking. ...

Employee Recognition.