Answer:

C. it will sell its products only to people who agree to buy only from it and not from rival firms.

Explanation:

Generally, any business can choose its business partners. But, under certain circumstances, there are limits on this freedom for a firm with a big market power.

There is an attempting to define those limited situations when this kinds of firm may violate antitrust law:

- The first option is that it violate the antitrust law by refusing to do business with other firms, or do business but under certain requisites. The key here is how the refusal to deal helps the monopolist maintain its empire, or allows the monopolist make an strategy where its monopoly is use in another market to attempt to monopolize other market.

- They can also refuse to deal with customers or suppliers, what cause the effect of preventing them from dealing with a rival: "If you deal with my competitor, I refuse to deal with you."

- Also, regarding to a firm dealing with its competitors, if the monopolist refuses to sell a product or service to a competitor and it makes it available to others, or if the monopolist has done business with the competitor and then stops, then the monopolist needs a legitimate business reason for its actions.

B bc it’s the right answer i just did it in my test

Answer:

The correct answer is: No, this situation is impossible.

Explanation:

To begin with, in the reality the situation with the demand curve is all the opposite. The <em>law of demand</em> establishes that there is an indirect relationship between the price of a product and its quantity demanded in the market, therefore that when the price of a good increases then its quantity demanded decreases. And it is by logic as well, because no one will buy more of something if the products is more expensive than it was before. Therefore that the situation in the text is impossible and it could only be opposite.

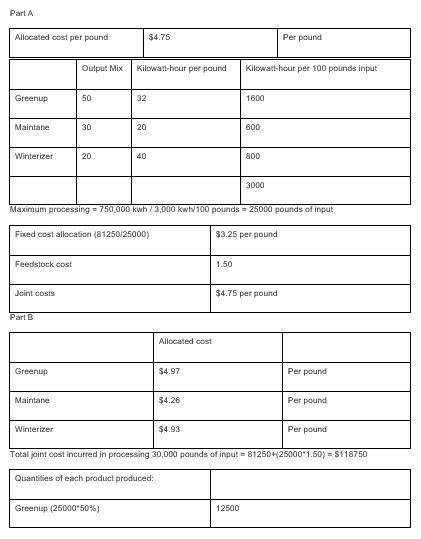

Answer:

See complete solution in the picture attachment.

Explanation:

Answer:

$800,579.28

Explanation:

The sum of the monthly payments can be found by the "annuity due" formula:

A = P(1 +n/r)((1 +r/n)^(nt)-1)

where P is the monthly deposit, r is the annual interest rate, n is the number of times per year it is compounded, and t is the number of years.

For this problem, we have ...

A = $400(1 +12/.06)(1(1 +.06/12)^(12·40)-1) = $400(201)(1 -1.005^480 -1)

A = $800,579.28

The account balance after 40 years will be $800,579.28.