Answer:

A. Qualified Business Income(QBI):- This is the Net income earned over and above the expenses. This is the business profit which is being earned over an accounting period. To calculate the QBI following are not considered

1. Interest Income 2. Income Earned Outside USA 3. Capital gain or Losses 4. Dividends and 5.Certain payments made to partners and Shareholders.

B. Qualified Business Income Deduction:- To calculate the QBI deduction the certain income limits have been defined. The QBI deduction is available at the rate of 20% of the QBI to the self employed and small business owners.

Single Filer- The limit in 2020 is $ 1,63,300 as Total Income

Joint filers- The Limit in 2020 is $ 3,26,600 as Total Income.

Since Haley does not qualify the Single Filer Limit as mentioned above, his QBI deduction is 0(Zero).

Explanation:

Option C

Organizational markets is another name for business-to-business markets

<h3><u>

Explanation:</u></h3>

B2B (business-to-business) marketing is retailing of goods to companies or another businesses for aid in making of goods, for application in usual business processes, or resale to different users, so as a wholesaler marketing to a retailer.

Business to business commits to trade that is carried within organizations, preferably than within a firm and personal customers. While buyers accept goods based not solely on cost but on reputation, rank, and additional sensitive triggers, B2B customers obtain judgments on value and gain inherent simply.

Answer:

The yearly economic cost for Fred's accounting business is $142,000.

Explanation:

Economic costs include both the explicit costs and the implicit costs.

Explicit costs are the expenditure on factors of production purchased from outsiders.

Implicit costs are the opportunity cost of owner provided resources.

Other expense is an explicit cost.

Foregone salary and foregone rent are the implicit costs.

So,

Economic cost = Foregone salary + Foregone rent + Other expenses

Economic cost = $95,000 + $22,000 + $25,000 = $142,000

Thus,

Answer:

Fraud-Late Filing Penalty

Explanation:

The tax infraction that incurs a penalty calculated as 15% of the amount of tax owed per month with a maximum penalty of 75% is the Fraud-Late Filing Penalty.

Fraud-Late Filing Penalty is the <u>penalty for filing late if a taxpayer did not file on time due to fraud</u>.

<u>The penalty is 15% of the amount of tax that should have been reported on the tax return</u> and an additional 15% for each additional month or part of a month that the taxpayer didn't file a return. <u>The penalty cannot exceed 75% of the unpaid tax.</u>

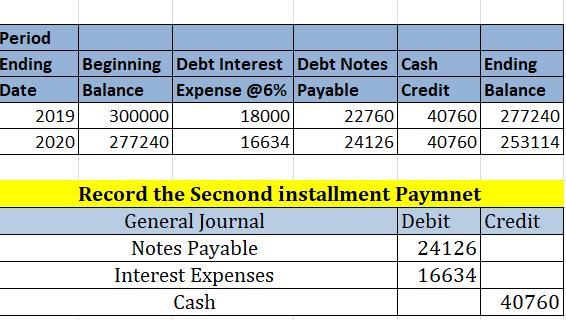

Answer:

debit interest expense of $16,634 , debit note payable $24,126 : Credit cash $40,760

Explanation:

Please attachment.