In order to help the

student expand his/her knowledge I will help answer the question. This in hope

that the student will get a piece of knowledge that will help him/her through

his/her homework or future tests.

The efforts to recruit

members of subordinate groups for jobs, promotions, or educational

opportunities are called affirmative action. The correct choice is letter

b. affirmative action

I hope it helps,

Regards.

<span> </span>

Answer:

Jan 22

Dr Cash $720,000

Cr Common stock $720,000

Feb 14

Dr Cash $2,420,000

Cr Preferred stock $2,420,000

30

Dr Cash $540,000

Cr Preferred stock $495,000

Cr Paid in capital in excess of par-Preferred stock $45,000

Explanation:

Preparation of the journal entries

Jan 22

Dr Cash $720,000

Cr Common stock $720,000

(180,000 shares * $4)

Feb 14

Dr Cash $2,420,000

Cr Preferred stock $2,420,000

(44,000 shares * $55)

30

Dr Cash $540,000

(9,000 shares * $60)

Cr Preferred stock $495,000

(9,000 shares * $55)

Cr Paid in capital in excess of par-Preferred stock $45,000

[9,000 shares *($60- $55) ]

Answer

Some of the hindrances of rational decision maker by managers are;

• Cognitive biases

• Time pressure

• Group conflict

Explanation

Decision making process is controlled by an individual’s personality and behavioral traits. Objective judgments by managers can be disrupted by subjective biases. Cognitive biases such as halo effect and overconfidence can act as a barrier to rational decision making.

Time pressure can distort the process of making a rational decision thus resulting to less objective individual judgment which is influenced by intuition. Managers with ample time arrive at a more logical and highly crafted decision than those who feel they have insufficient time.

Both interpersonal and group dynamics can create a barrier towards making an effective decision.

The Vatican's swiss guard wears a uniform inspired by famous renaissance painter Raphael.

<h3>Who is the Swiss guard?</h3>

Since 1506, the Swiss Guard has provided protection to the Pope and his home, and this has not been modified. These men also share a desire to learn more about the most recent developments and practices in personal security, as well as a sense of discovery on the international stage.

Raphael (1483-1520 CE) was a painter and architect from Italian background who is considered one of the greatest Renaissance artists. Raphael produced a large body of work in the medium of oil painting, including a large number of masterpieces.

Learn more about the swiss guards, here:

brainly.com/question/22952265

#SPJ1

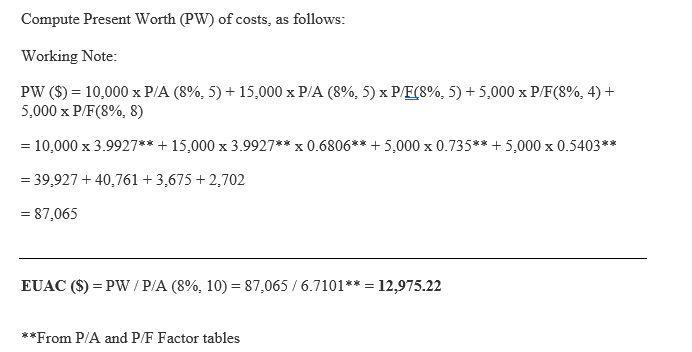

Answer

The answer and procedures of the exercise are attached in the image below.

Explanation

Please consider the data provided by the exercise. If you have any question please write me back. All the exercises are solved in a single sheet with the formulas indications.