The answer is C.) Technical

Answer

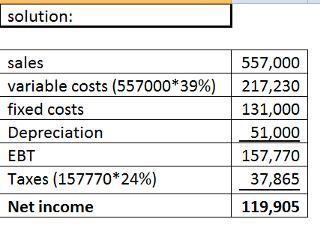

The answer and procedures of the exercise are attached in the following archives.

Explanation

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

Answer: Williamson industries would have obtained $7.78 billion in sales

Explanation: According to the question, the company is having a total of $2 billion in fixed assets. The fixed assets are currently operating at 90% (0.9) of its total capacity. At his level, the company is able to achieve a sales figure of $7 billion. The implication is as follows;

Fixed assets (at 100%) = 2 billion

Fixed assets (at 90%) = 2 * 0.9

Fixed assets (at 90%) = 1.8

If the company utilizes $1.8 billion to achieve a $7 billion sales figure, then operating at full capacity (100%) would yield the following;

7/x = 90/100

(Where x equals sales level at 100% capacity)

7/x = 0.9

Cross multiply

x = 7/0.9

x = 7.7777...

x ≈ 7.78

Therefore, if Williamson Industries had been operating at full capacity, it would have obtained a sales level of $7.78 billion

Answer:

a. retained earnings of the seller are overstated

Explanation:

An asset transfer from a subsidiary to its parent at a gain is an Intragroup transaction. Intragroup transactions must be eliminated otherwise the financial statements would be misleading and not have a faithful representation.

The consequence of this transfer is that the Income of the Seller (subsidiary) increases and this also increases the Retained Income Balance of for the Subsequent years. We should eliminate this Income.