Answer: d. all of these answer choices are correct

Explanation:

Available for sale securities are held by a firm with the intention of selling it before it reaches its maturity date.

So as not to report on the income statement wrongly, the Unrealized gains(losses) which are any fluctuations from the original price, throughout the Security's lifetime is posted to the Other Comprehensive Income account in the Equity section of the balance sheet. That along with the Realized gains when the security is sold.

Reclassification adjustments are also included to account for the reclassification of a security to either a profit or a loss.

All of the above are correct.

The correct answer to this question is this one: "C. Finance Charge." <span>Collectively, the interest costs and other fees for using a credit card called the finance charge. IT has something to do with the charges after you used the credit cards.</span>

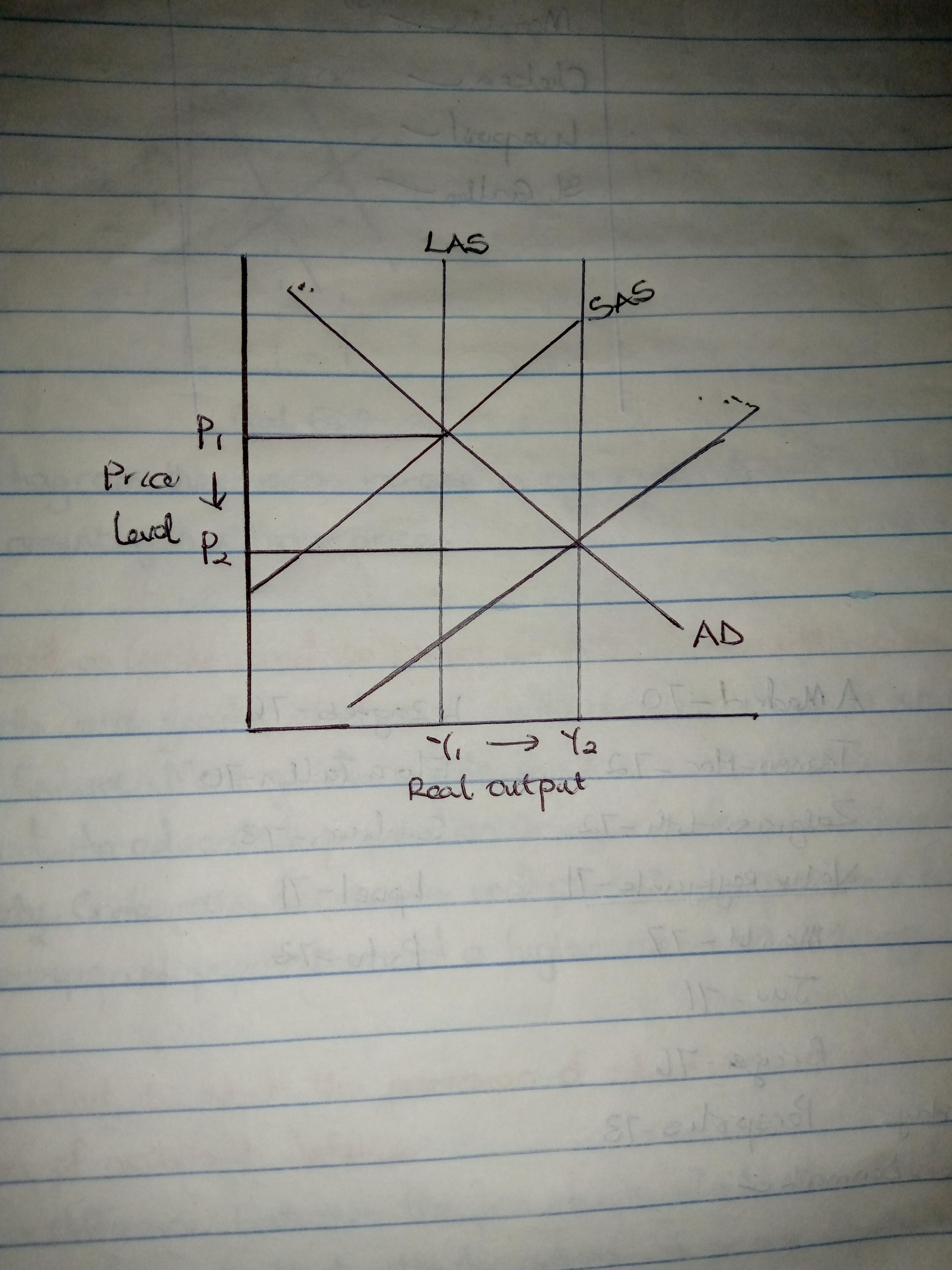

Answer: The price level falls and output rises.

Explanation:

According to Moore's law, it is stated that the computing speed of a microchip doubles every 18 months. According to Moore, this will increase thespeed and capability of computers and also bring about lesser pay for the computers.

The effect of this on the economy is that it will lead to a fall in price level and increase in output as there will be faster and cheaper production. This can be shown in the diagram attached.

The proceeds that UWD received will be as follows:

Number of shares 1,350,000

share price $24.62

Amount realized from the shares:

1,350,000×24.62

=33,237,000

Total amount to be deducted will be:

(Commission+Accounting fees+legal fees+printing costs+selling expenses)

commission=$1,661,850

Accounting fees=$450,000

legal fees=$1,225, 000

printing cost=$275,000

selling expenses=$300,000

Total=(1,661,850+450,000+1,225,000+275,000+300,000)

=$3,911,850

The amount received will be:

33,237,000-3,911,850

=$29,325,150