Answer:

IKIBAN INC.

Statement of cash flow using indirect method for

the year ended June 30, 2019

Particulars Amount

$

Cash flow from operating activities

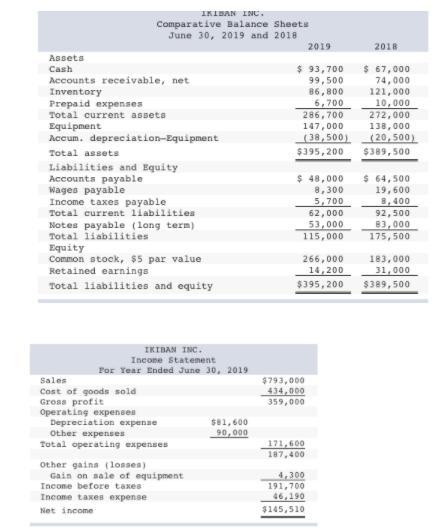

Net Income 145,510

<em>Adjustments to reconcile net income to net</em>

<em>cash provided by operating activities

</em>

<u>Adjustment for non cash effects</u>

Depreciation 81,600

Gain on sale of equipment -4,300

<u>Change in operating assets & liabilities</u>

Increase in accounts receivable -25,500

Decrease in inventory 34,200

Decrease in prepaid expenses 3,300

Decrease in accounts payable -16,500

Decrease in wages payable -11,300

Decrease in income taxes payable <u>-2,700 </u>

Net cash flow from operating activities (A) 204,310

Cash Flow from Investing activities

New equipment purchased -80,600

Equipment sold <u>12,300</u>

Net cash Flow from Investing activities (B) -68,300

Cash Flow from Financing activities

Cash dividends paid -162,310

($31,000 + $145,510 - $14,200)

Common stock issued 83,000

Notes payable paid <u>-30,000</u>

Net cash Flow from Financing activities (C) -109,310

Net Change in cash = A+B+C $26,700

($204,310 - $68,300 - $109,310)

Beginning cash balance <u>$67,000</u>

Closing cash balance <u> $93,700</u>