Answer:

The effect the entry to recognize the uncollectible accounts expense for Year 2 will have on the elements of the financial statements are that it will reduce Accounts Receivable to $15,560 and the Allowance for Doubtful Accounts to $1,900 at the end of Year 2.

Explanation:

Credit sales estimated to be uncollectable = Credit sales * Estimated percentage uncollectable = $215,000 * 1% = $2,150

Ending account receivable = Beginning accounts receivable + Credit sales - Cash collected - Receivales written off as uncollectable - Credit sales estimated to be uncollectable = $76,000 + $215,000 - $271,100 - $2,100 - $2,150 = $15,560

Ending Allowance for Doubtful Accounts = Beginning Allowance for Doubtful Accounts - Allowance for Doubtful Accounts - Receivales written off as uncollectable = $4,000 - $2,100 = $1,900

Therefore, the effect the entry to recognize the uncollectible accounts expense for Year 2 will have on the elements of the financial statements are that it will reduce Accounts Receivable to $15,560 and the Allowance for Doubtful Accounts to $1,900 at the end of Year 2.

Answer: $33,400

Explanation:

The annual depreciation using the straight-line method is;

= (Cost - Residual value) / Useful life

= (45,200 - 3,900) / 7

= $5,900

On December 31, 2020, the vehicle would have depreciated by 2 years so the book value would be;

= Cost - Accumulated depreciation

= 45,200 - (5,900 + 5,900)

= $33,400

It is true that capitalization of interest is adding accrued interest to the principal balance, so that the interest-bearing principal balance of the loan increases.

<h3>What is interest capitalization?</h3>

This is when an unpaid interest is rolled over with the principal amount, which increase the overall amount to be paid. It is the inclusion of an unpaid interest to the principal balance of the loan taken.

Hence, Capitalization of interest is adding accrued interest to the principal balance, so that the interest-bearing principal balance of the loan increases.

Learn more about interest capitalization here: brainly.com/question/417585

#SPJ1

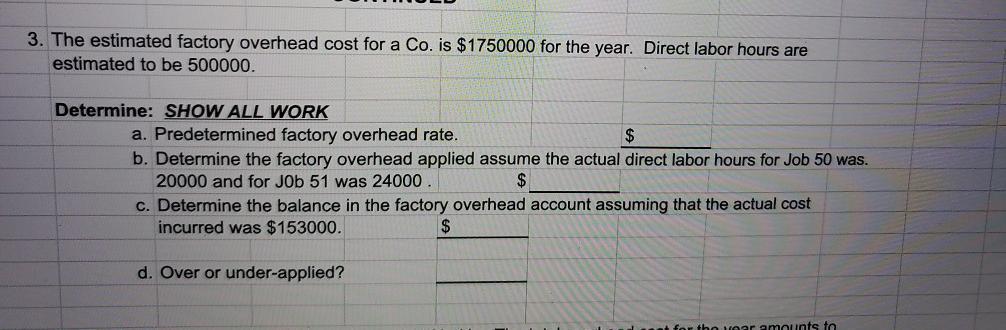

Answer:

Note <em>See complete question as attached as picture below</em>

<em />

a. Predetermined factory overhead rate = Estimated factory overhead cost / Direct labr hours

Predetermined factory overhead rate = $1,750,000 / 500,000 hours

Predetermined factory overhead rate = $3.50 per direct labor hours

b. Particulars Amount

Job 50 (20,000*3.50) $70,000

Job 51 (24,000*3.50) <u>$84,000</u>

Factory overhead applied <u>$154,000</u>

c. Balance in factory overhead = $154,000 - $153,000

Balance in factory overhead = $1,000

d. Over-applied factory overhead = $1,000