Answer:

This is the Predetermined overhead rate

Explanation:

The predetermined overhead rate assigns a particular amount of manufacturing overhead to each direct labor or machine hour. This helps businesses allocate resources and also set pricing. This computation is usually done at the beginning of each period.

To calculate this, we divide the estimate of the manufacturing overhead cost total by the estimated number of machine hours. It is used to assign overhead cost to jobs.

Answer:

8%

Explanation:

The formula and the computation of the price elasticity of supply is shown below:

Price elasticity of supply = (Percentage change in quantity supplied ÷ percentage change in price)

where,

Price elasticity of supply = 0.4

And, the percentage change in price = 20%

So, the percentage change in quantity supplied is

= Price elasticity of supply × the percentage change in price

= 0.4 × 20%

= 8%

It shows a direct relationship between the quantity supplied and the price.

Answer:

c. protect lessees against lessors who abuse leased assets.

Explanation:

The residual value guarantee may be defined as a guarantee that is made to the lessor where the value of an underlying asset will become at least some specified amount at the end of the lease. The guarantee is given by the party unrelated to a lessor.

The residual value guarantee provides to protect the lessor against the lessees who tries to abuse the leased assets. It does not protect the lessees against the lessors.

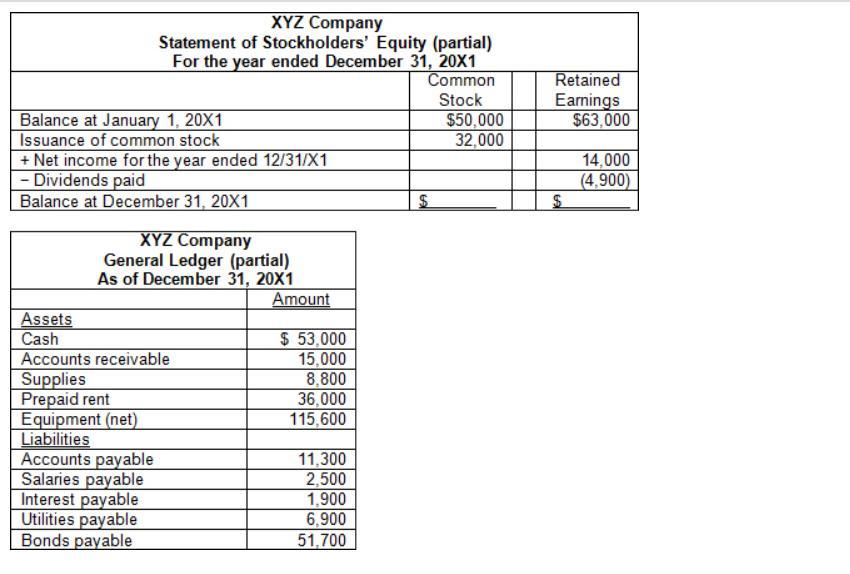

Answer:

$112,800

Explanation:

The computation of the total amount of current asset reported is as follows:

= Cash + account receivable + supplies + prepaid rent

= $53,000 + $15,000 + $8,800 + $36,000

= $112,800

Hence, the amount reported is $112,800

We simply added the above four items so that the current asset value could come

Answer:

(1) 6%; 1.7; 10.20%

(2) 3%; 4; 12%

Explanation:

ROI = Margin × Turnover (Note Margin in % and Turnover in Ratio)

Where,

Margin = Net operating income ÷ Sales

Turnover = Sales ÷ Average operating assets

For Queensland:

Margin = 54,060 ÷ 901,000

= 6% (approx)

Turnover = 901,000 ÷ 530,000

= 1.7

ROI = 6% × 1.7

= 10.20%

For New south wales:

Margin = 74,400 ÷ 2,480,000

= 3% (approx)

Turnover = 2,480,000 ÷ 6,20,000

= 4

ROI = 3% × 4

= 12%