Answer:

b. 502,000 units

Explanation:

- X

Desired Ending 34,000

R1 320,000

R2 180,000

Beginning (32,000)

Production Budget 502,000

32,000 + P = 34,000 + (320,000 + 180,000)

34,000 + 320,000 + 180,000 - 32,000 = 502,000 = Production

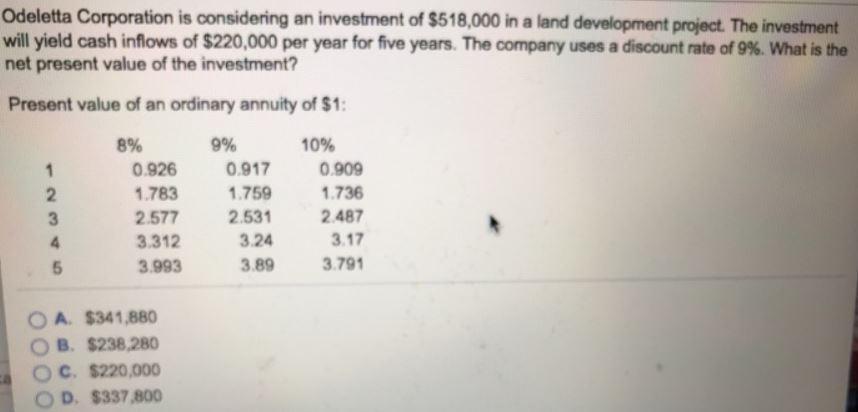

Answer: $337,800

Explanation:

Cashflow is constant so is an annuity.

The Present value of the Investment;

= Present Value of Cashflow - Investment cost

= (220,000 * Present value interest factor of an annuity, 5 years, 9% ) - 518,000

= (220,000 * 3.89) - 518,000

= 855,800 - 518,000

= $337,800

Answer:

$ 358,063

Explanation:

Calculation for the amount that Ruby's IRA will be worth when she needs to start withdrawing money from it when she retires.

Ruby's IRA worth when she retires at age of 65

First step

Using this formula to find how many years until Ruby retires

Time period= Retired age (-) current age

Let plug in the formula

65-25=40 years

Second step is to find the future value of IRA when she retires

Using this formula

Future value of IRA when she retires

= Present value(1+r)t

Let plug in the formula

$ 11,400 (1+0.09) ^40

=$11,400 (1.09) ^40

=$ 11,400 (31.409)

= $ 358,063

Therefore the amout that Ruby's IRA will be worth when she needs to start withdrawing money from it when she retires will be $358,063

We need the is as follows to know and answer the question sorry but can hellp unless the questions finished