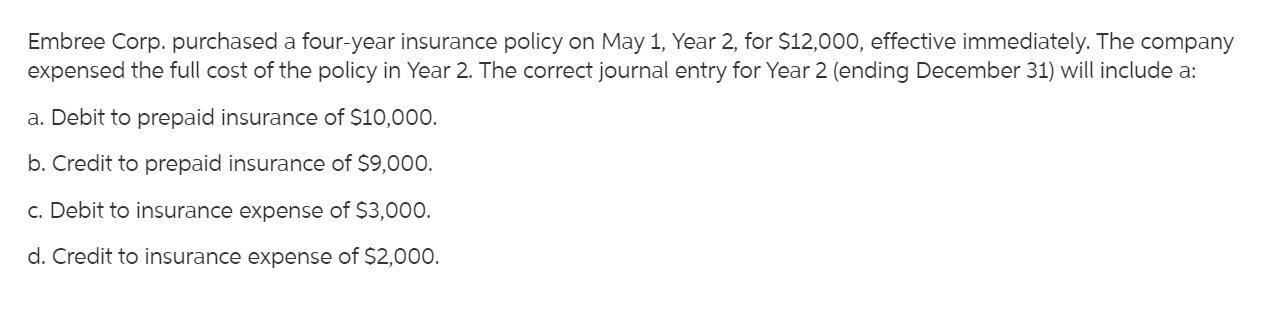

Answer:

a. Debit to Prepaid Insurance of $10,000

* Option for this question was missing so I have attached a similar question with this answer and answered accordingly.

Explanation:

Insurance purchased for four years was actually prepaid insurance on May 1, Year 2.

The company expensed all amount by positing following entry ( which is a wrong entry)

DR. Insurance Expense $12,000

Cr. Cash $12,000

It should be entered as follow:

DR. Prepaid Insurance $12,000

Cr. Cash $12,000

At the end of the year 2 8 months has been passed for which $2,000 is accrued and it will be recorded, as all the amount is charged to the expense account we will adjusted the remaining amount of $10,000 to correct this mistake.

Now at the end of year 2 the correct entry which will settle the expense and prepaid insurance as well is as follow.

DR. Prepaid Insurance $10,000

Cr. Insurance Expense $10,000