Answer:

$2,000

Explanation:

From the question, the initial tax basis of Rubio is $20,000.

In a partnership, share of profit will increase the initial basis while share of loss will reduce it.

As the share of Rubio in the limited partnership loss for the year is $22,000, it will make his tax basis to fall to zero because the loss of $22,000 is greater than his tax basis. The amount by which the loss is greater than his tax basis, i.e. $2,000 ($22,000 - $20,000) will be the loss that is allowed considering only the tax basis loss limitations.

Therefore, $2,000 loss is allowed to be carried over due only to the tax basis loss limitation.

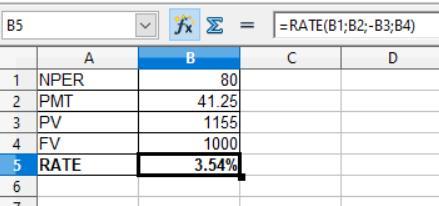

Answer:

4.96%

Explanation:

In order to determine the component after-tax cost of debt first we need to compute the before tax cost of debt by applying the RATE formula which is to be shown in the attachment below:

Given that,

Present value = $1,155

Future value or Face value = $1,000

PMT = 1,000 × 8.25% ÷ 2 = $41.25

NPER = 40 years × 2 = 80 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after applying the above formula

1. The pretax cost of debt is 3.54% × 2 = 7.08%

2. And, the after tax cost of debt would be

= Pretax cost of debt × ( 1 - tax rate)

= 7.08% × ( 1 - 0.30)

= 4.96%

Answer:

portfolio's standard deviation = 6.18%

Explanation:

we must first determine the expected returns for each stock:

stock A = (0.15 x 31%) + (0.6 x 16%) + (0.2 x -3%) + (0.05 x -11%) = 13.1%

stock B = (0.15 x 41%) + (0.6 x 12%) + (0.2 x -6%) + (0.05 x -16%) = 11.35%

stock C = (0.15 x 21%) + (0.6 x 10%) + (0.2 x -4%) + (0.05 x -8%) = 7.95%

then we must determine the variance of each stock's return:

stock A = {[0.15 x (31 - 13.1)²] + [0.6 x (16 - 13.1)²] + [0.2 x (-3- 13.1)²] + [0.05 x (-11 - 13.1)²]} / 4 = (48.0615 + 5.046 + 51.842 + 29.0405) / 4 = 33.4975

stock B = {[0.15 x (41 - 11.35)²] + [0.6 x (12 - 11.35)²] + [0.2 x (-6- 11.35)²] + [0.05 x (-16 - 11.35)²]} / 4 = (131.868375 + 0.2535 + 60.2045 + 37.401125) / 4 = 57.4219

stock C = {[0.15 x (21 - 7.95)²] + [0.6 x (10 - 7.95)²] + [0.2 x (-4- 7.95)²] + [0.05 x (-8 - 7.95)²]} / 4 = (25.545375 + 2.5215 + 28.5605 + 12.720125) / 4 = 17.3369

portfolio's variance = (0.3 x 33.4975) + (0.4 x 57.4219) + (0.3 x 17.3369) = 38.21908

portfolio's standard deviation = √38.21908 = 6.18%

Max is a waiter at a coffee shop. He gets paid $100 every day at 9 p.m. regardless of the number of customers he serves during the day. In this scenario, max's payment is based on the fixed-interval schedule. Hence, option C is correct.

<h3>What is fixed-interval schedule?</h3>

In fixed-interval schedules, the first reaction is only rewarded when a predetermined amount of time has passed. With this schedule, reactions are quicker toward the end of the interval but slower immediately following the reinforcement.

A child may receive a candy as part of a fixed-ratio program after reading three to ten pages of a book.

Thus, option C is correct.

For more details about fixed-interval schedule, click here:

brainly.com/question/12282349

#SPJ4

The options are missing-

a. fixed-ratio schedule

b. variable-interval schedule

c. fixed-interval schedule

d. variable-ratio schedule

Answer:

C. managing broker over Agent Smith

Explanation:

a managing broker is someone is held liable over the actions of another broker office or agency that act on the managing broker's behalf. Thse office or agnecy are allowed to act without direct order from the managing broker, but managing broker will be the one that receive all the consequences.

All the profit that is made by managed entity (in this context agent smith) will have to goes to managing broker first and the managing broker will share the profit on a private term with Agent Smith.

In return, the managing broker will have to ensure that all of the agents that he/she has under disposal have to follow the compliance rule that is made by the government. He will manage the licence and annual tests of the agents in order to ensure consumer safety.