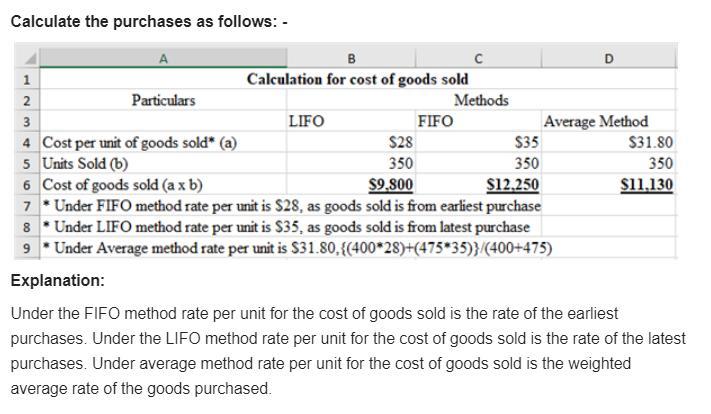

Answer:

1,2- See attached pictures.

3-

1. LIFO

2. Average

3. FIFO

Explanation:

See attached pictures.

Answer:

True

Explanation:

This is one of the major reason why companies expands its manufacturing department in countries with greater free trade agreements and with geographical importance. This makes the company more oriented towards controlling transportation costs, import duties and other costs and increasing the benefits arising from the economies of scale.

Rent, expenses made by office, telephone expenses, administrative salaries are the items that fall under indirect cost.

Explanation:

Indirect costs are those cost which are not accountable directly. Indirect cost can be either variable or fixed. Indirect cost are also known as overhead expenses.

Rent can act as both direct as well as indirect cost. If rent is given for the plant as well as machinery for a company which is use by manufacturing units directly fall under direct cost but in other way when the rent is given for various official purposes it will fall under indirect cost.

Answer:

Cost of equity = 10.5%

Explanation:

<em>The capital asset pricing model is a risk-based model. Here, the return on equity is dependent on the level of reaction of the the equity to changes in the return on a market portfolio. These changes are captured as systematic risk. The magnitude by which a stock is affected by systematic risk is measured by beta. </em>

Under CAPM, Ke= Rf + β(Rm-Rf)

Rf-risk-free rate (long-term i.e 10 year treasury bill rate), β= Beta, Rm= Return on market., Ke- Return on equity (cost of equity)

This model can be used to work out the cost of equity as follows:

Ke= Rf + β (Rm-Rf)

Rf- 6%, β= 1.0, Rm- 10.5, E(r)- ?

Ke = 6% + 1.0× (10.5 -6)% = 10.5%

Ke = 10.5%

Cost of equity = 10.5%

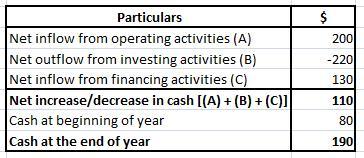

Answer:

$190

Explanation:

‘Cash Flow Statement’ is one of major financial statement that indicates the inflow and outflow of cash along with the reasons by categorizing each cash transaction in three activities i.e., operating, investing or financing activity. Non-cash transactions are not considered while preparing a cash flow statement.

Given,

Net inflow from operating activities (A) = $200

Net outflow from investing activities (B) = ($220)

Net inflow from financing activities (C) = $130

Cash at beginning of year = $80

Now,

Net increase/decrease in cash = (A) + (B) + (C)

Net increase/decrease in cash = $200 + ($220) + $130

Net increase/decrease in cash = $110

Cash at the end of year = Net increase/decrease in cash + Cash at beginning of year

Cash at the end of year = $110 + $80

Cash at the end of year = $190

Cash flow statement has been attached below: