Answer:

Data consolidation.

Explanation:

Data consolidation involves the gathering, collection and storage of data in a single place.

Data consolidation helps an organisation in the reduction of costs because the business will have no need for purchasing different hardwares such as routers and servers.

Data consolidation helps to improve the security system of the organisation by protecting it from various forms of cyberattacks.

Answer: See explanation

Explanation:

The flotation cost adjustment that must be added to its cost of retained earnings will be calculated thus:

= Expected dividend / [Current price × (1 - Floatation cost)] + Expected growth rate

= 2.00/[20.00 × (1 - 4.5%)] + 4.2%

= 2.00 /[20.00 × (1 - 0.045)] + 0.042

= 2.00 / (20.00 × 0.955) + 0.042

= (2.00/19.10) + 0.042

= 0.104712 + 0.042

= 0.146712

New cost of equity = 14.67%

You didn't give the cost of equity calculated without the flotation adjustment. Let's assume that this is maybe 11%, the floatation on adjustment factor = 14.67% - 11% = 3.67%

Answer:

Net Income Bargain Electronics would realize by accepting the special order is - $ 24,000

Explanation:

Bargain Electronics is operating at full capacity, therefore the fixed costs are relevant at this decision.

<u>Incremental Costs and Revenues - Special Order 3000 units</u>

Sales ( 3000 × $25) 75,000

Variable Cost (3000× $20) (60,000)

Fixed Costs (3000× $10) (30,000)

Shipping Costs ( 3000×$3) (9,000)

Net Income -24,000

Answer:

O expansionary fiscal policy

Explanation:

Point C represents a recession. During a recession, the economy experiences slow or negative growth. The unemployment rate is way above the recommended levels. The economy requires stimulation to accelerate growth and create job opportunities.

Congress controls the fiscal policies in the US. Fiscal policy is about adjusting taxation and government spending. Expansionary fiscal policies accelerate economic growth in a country. These policies target to income the amount of money in circulation. Reductions of taxes and an increase in government are expansionary.

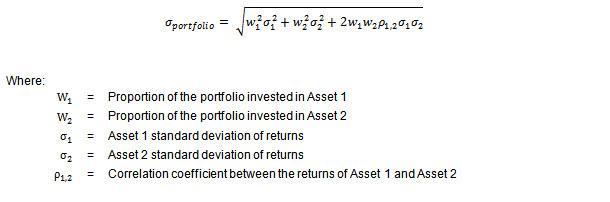

Answer:

Portfolio Mean = 7.2%

Portfolio Stdev = 0.1169615 or 11.69615% rounded off to 11.70%

Explanation:

The mean return of a portfolio consisting of two securities can be calculated by multiplying the weight of each security in the portfolio by the mean return of that security and adding the products for each security. The formula for two asset or security portfolio return (mean) can be written as follows,

Portfolio Mean = wA * rA + wB * rB

Where,

- w represents the weight of each security

- r represents the mean return of each security

Portfolio Mean = 60% * 8% + 40% * 6%

Portfolio Mean = 7.2%

The standard deviation is a measure of the total risk. The standard deviation of a portfolio consisting of two securities can be calculated using the attached formula.

Portfolio Stdev = √(0.6)² (0.2)² + (0.4)² (0.15)² + 2(0.6) (0.4) (-0.3) (0.2) (0.15)

Portfolio Stdev = 0.1169615 or 11.69615% rounded off to 11.70%