Answer:

1. Enhanced customer service.

2. Employee retention.

Explanation:

1. Enhanced customer service - motivated employees always take ownership of their job. In hospitality, it is important to provide best quality customer service. Having motivated employees mean employees are ready to serve customers in the best possible way.

2. Employee retention - since a new hotel has just opened up, they will be looking for hiring people locally, to retain her current employees it is important for Sasha to keep her employees motivated.

Answer: D.Returning inventory that is defective or broken. (happy to help)

Explanation:

Answer:

Ending inventory will be $108925

Explanation:

We have to find the estimated ending inventory

It is given by

Estimated ending inventory = Cost of Goods available for sale - Cost of Goods Sold

Cost of Goods available for sale = $155,000+$467,300 = $622,300

Cost of Goods Sold = Sales - Gross profit =

So ending inventory = $622300 - $513375 = $108925

So ending inventory will be $108925

Complete Question

The complete question is shown on the first uploaded image

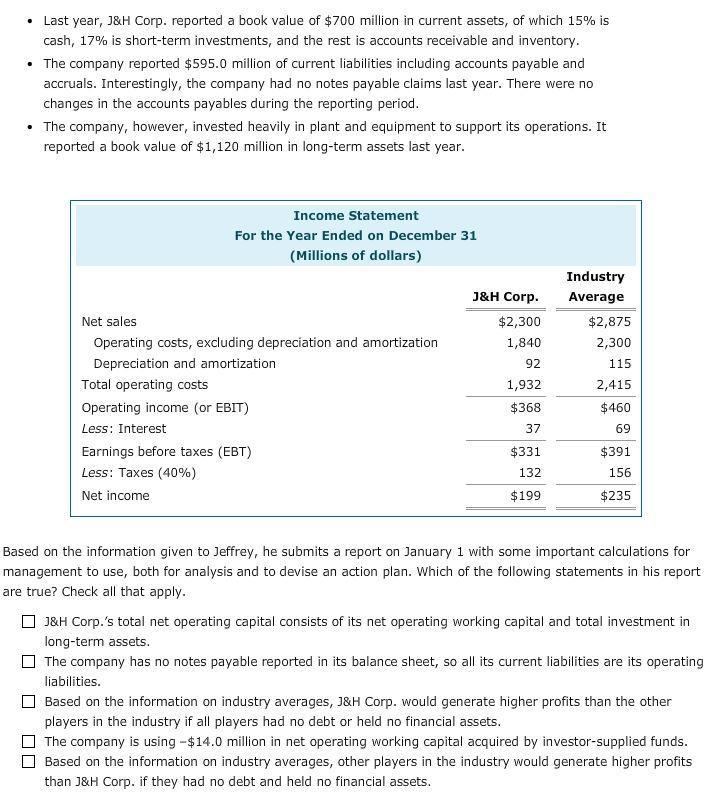

Answer:

The correct stalemates are

The company is using -$14 million in net operating working capital

acquired by investor supplied funds.

Based on the information on industry averages , other players in the industry

would generate higher profits than J&H Corp , if they had no debt and

held no financial assets

Explanation:

The calculation is shown on the second and third uploaded image

What is the question you are asking