Answer:

d) $6,000, -$6,000

Explanation:

Accounting profit = total revenue - explicit costs

=6000 x 2.5-9000 = $6000

Economic profit = accounting profit - interest on capital invested

=6000 - 400000 x 0.03

=$-6000

Answer: Upward distortion

Explanation:

According to the given question, Daniel gave an excellent idea for his organization that helps in increase the productivity and the growth of the company.

The Daniel's original ideas sent to the manager and the superior of the company and then at that level his idea star filtering and become ineffectual and this occurrence is called as upward distortion.

In an organization their is occurrence of distortion in the upward level of communication and the information or message get distorted. Therefore, Upward distortion is the correct answer.

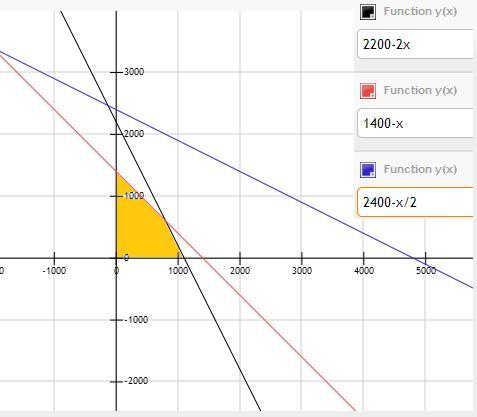

Answer:

Consider the following calculations

Explanation:

Let X be Bagels and Y be croissants

Profit:

20X+30Y

Subject:

6X+3Y<=6600

1X+1Y<=1400

2X+4Y<=4800

Critical points are

(0,1400) , (800,600) , (1100,0)

So

Max at 0,1400 and P =4200