Answer:

<u></u>

- <u>That the career you choose might decline in the future and your knowledge and train could be not valuable then.</u>

Explanation:

Your criteria, interests, points of view, and even opportunities could change in the medium or long term.

Most likely, many the jobs of the future, which we do not even imagine that can exist, will require new skills.

The best skill that you can learn today is to learn: learn to learn.

You should be prepared to learn different things from many fields. Thus, your best decision today is to be broad your opportunities instead of narrowing them.

The danger of limiting your career opportunities to only those you have heard about or been trained for is that the job opportunites, in the career you choose, might decline in the future and you would count with a baggage of good knowledge and train that would not be valuable, because that kind of job is no longer required.

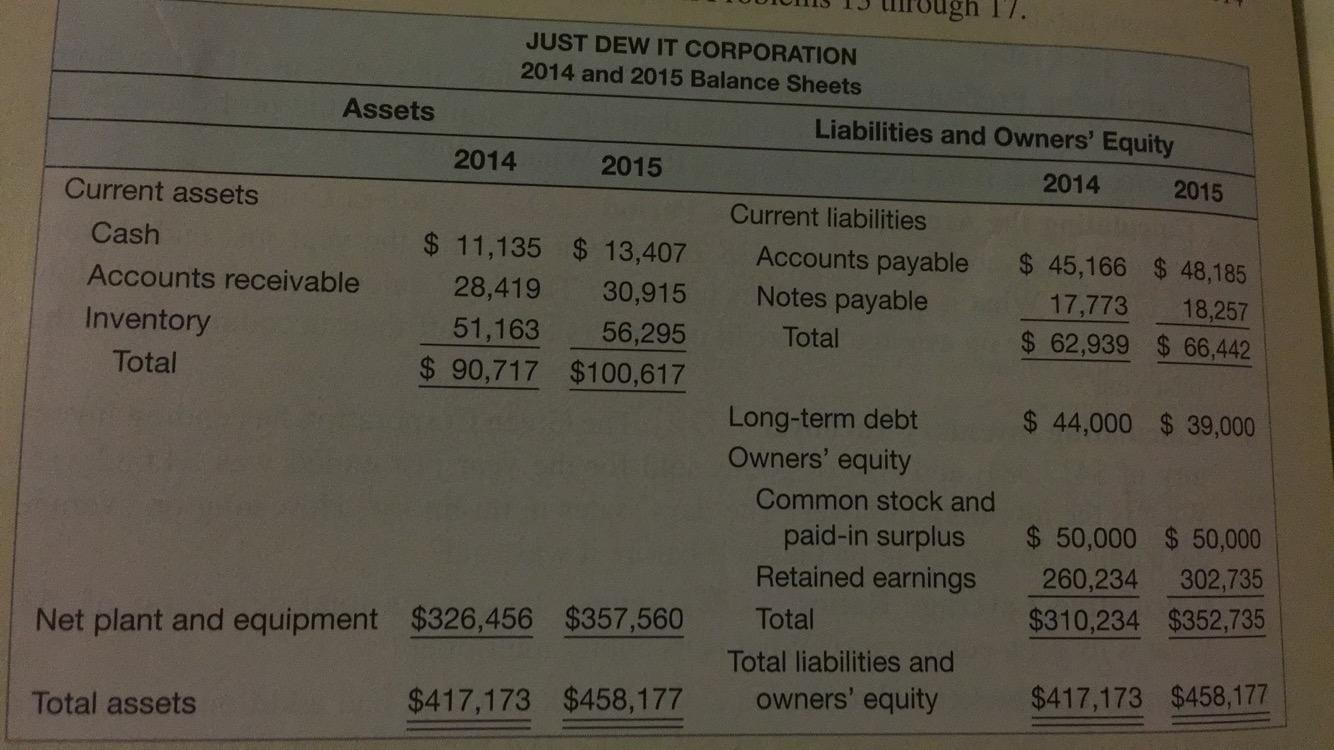

Answer:

a. Current ratio = current assets / current liabilities

- 2014 = $90,717 / $62,939 = 1.44

- 2015 = $100,617 / $66,442 = 1.51

b. Quick ratio = (current assets - inventory) / current liabilities

- 2014 = ($90,717 - $51,163)/ $62,939 = 0.63

- 2015 = ($100,617 - $56,295)/ $66,442 = 0.67

c. Cash ratio = (cash + cash equivalents) / current liabilities

- 2014 = $11,135 / $62,939 = 0.18

- 2015 = $13,407 / $66,442 = 0.20

d. NWC to total assets ratio = net working capital / total assets

- 2014 = $27,778 / $417,173 = 0.07

- 2015 = $34,175 / $458,177 = 0.07

e. Debt-equity ratio = total debt / total equity

- 2014 = $106,939 / $310,234 = 0.34

- 2015 = $105,442 / $352,735 = 0.30

equity multiplier = total assets / total equity

- 2014 = $417,173 / $310,234 = 1.34

- 2015 = $458,177 / $352,735 = 1.30

f. Total debt ratio = liabilities / assets

2014 = $106,939 / $417,173 = 0.26

2015 = $105,442 / $458,177 = 0.23

long-term debt ratio = long term liabilities / assets

- 2014 = $44,000 / $417,173 = 0.11

- 2015 = $39,000 / $458,177 = 0.09

I had to look for the options and here is my answer:

According to the Dividend Growth Model, a decline in the DISCOUNT RATE will increase the stock's current value. The Dividend Growth Model, or also known as the <span>Gordon </span><span>Growth Model, is the basis in the calculation of the intrinsic value of a stock not including any conditions of the current market.</span>

An automatic investment plan would be the service offered to an investor for him/her to earn a compound interest in its investments. Also known as AIP, the amount would be deducted automatically to the savings bank account of the investor so that the fund would be added to its retirement plan.

The inequality is:

18 + 6 x > 80

6 x > 80 - 18

6 x > 62

x > 62 : 6

x > 10.333... miles

She would need to ride her bicycle more than 10 1/3 miles each day to achieve her goal.