Answer:

$44,592

Explanation:

The book value of a building = Cost Price - Accumulated Depreciation

= $(251,060 - 109,510)

= $141,550

The present value of the non-interest-bearing note due on January 1, 2023 (or Discounted Cash Flow) =

FV/(1+i)^t

= $241,060/(1+0.09)^3

= $241,060/1.29503

= $186,142

Gain on Sale of the building = $(186,142 - 141,550) = $44,592

Bank reconciliation refers to looking at your bank statement and your personal register and making sure they match up with no discrepancies. In this case, there were discrepancies, $150 worth so John had to look and see what was missing and making sure they both equaled the same amount. From the numbers given, John's bank account was reconciled $150.

Answer:

$30,600

Explanation:

Accounts receivable should comprise the total amount of cash from sales during the quarter and the amount of credit sales collected during the quarter in question, so the 20% to be collected in the following quarter shouldn't be represented in this budgeted sheet. Assuming that cash and credit payments represent the totality of net sales, accounts receivable for the quarter can be represented as follows:

Jericho would report $30,600 on the budgeted balance sheet.

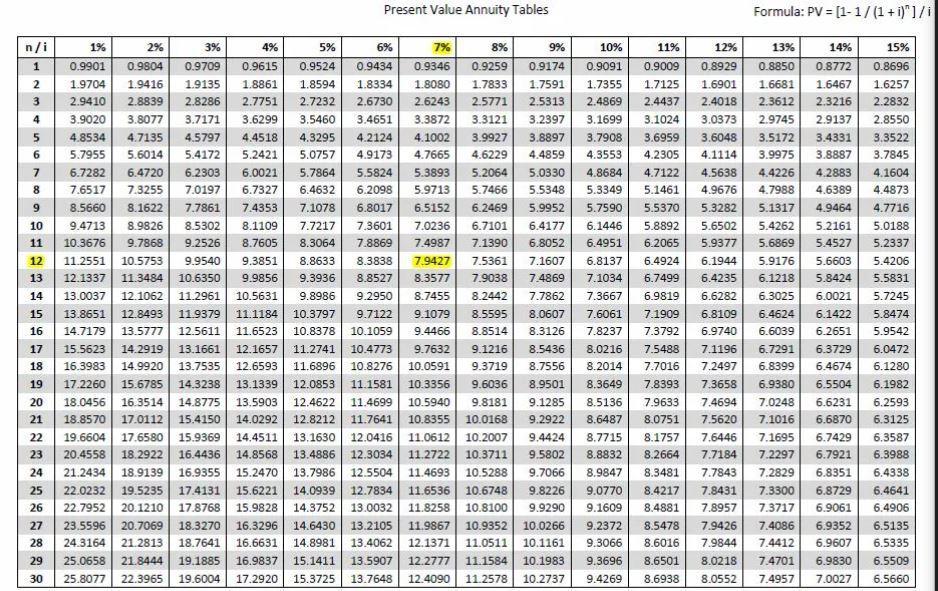

Answer: $80 million per year for 25 years

Explanation:

The option you should choose is one that will guarantee you the highest present value.

This means that you need to discount the annual payment of $80 million per year for 25 years to find the present value. As you did not include a rate, we shall assume a rate of 8% for reference purposes.

The annual payment is an annuity so the present value can be calculated by:

Present value of annuity = Annuity payment * Present value interest factor, rate, no. of years

= 80,000,000 * Present value interest factor, 8%, 25 years

= 80,000,000 * 10.6748

= $853,984,000

<em>The present value of the annual payment is more than the present value of the $850 million received today so the Annual payment should be taken. </em>

Answer:

Explanation:

The preparation of the Cash Flows from Operating Activities—Indirect Method is shown below:

Cash flow from Operating activities - Indirect method

Net income $149,000

Adjustment made:

Less: Gain on the sale of land -$12,000

Less: Increase in accounts receivable -$19,000

Less: Increase in inventory -$12,000

Less: Decrease in accounts payable -$39,000

Total of Adjustments -$82,000

Net Cash flow from Operating activities $67,000