Answer: 0.80:1

Explanation:

Given that,

Cash balance = $80,000

Short-term investments = $20,000

Net receivables = $60,000

Inventory = $450,000

Current liabilities total = $200,000

Quick assets = Cash balance + Short-term investments + Net receivables

= $80,000 + $20,000 + $60,000

= $160,000

Red Line’s quick ratio =

=

= 0.80 : 1

Answer:

Final Accounts Receivable $ 3191

Explanation:

Opening Accounts Receivable $3,200

Received Cash Payment $ 9

Ending Accounts Receivable $3200- $ 9= $ 3191

Opening Cash $12,100

Received customer payment $ 9

Bought manufacturing supplies $ 17

Sold inventory at cost $ 25

Ending Cash Balance = $2100 + 9-17 + 25= $ 2117

<h2><u>Accounts Receivable </u></h2><h3><u>Debit Credit</u></h3>

Opening $3,200

Cash Received 9

<u> Ending $ 3191</u>

<u>$3200 $3200 </u>

The only receipt is of $ 9 which is deducted from the opening accounts receivable to get the final account receivable.

Answer is Capital Budgeting

Reason

Evaluating and planning for long term investments and risk of future cash flows is capital budgeting.

Answer:

Following are the responses to the given choices:

Explanation:

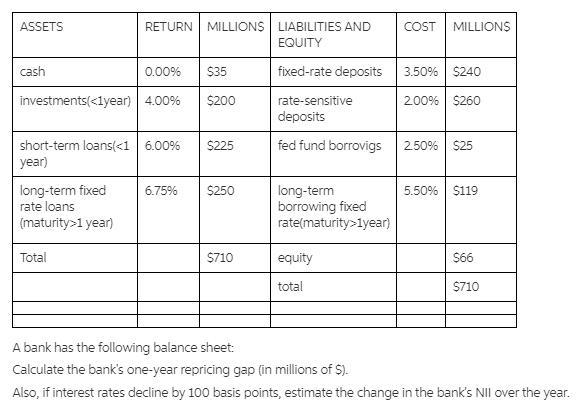

Please find the complete question:

1-year distance recovery = sensitive resources rate - liabilities sensitive rate

Rate sensitive assets = investments(<1 year) + short-term loans(<1 year)

Dependent Rate=sensitive rate of deposits+ fed fund borrowing

The difference in replicating gaps:

If interest rates decline by 1%, net income becomes down

Answer:

recasting

Explanation:

"Recasting" is a type of caregiver strategy that allows the caregiver to repeat what the kid/learner is trying to say. This is done in a manner of <em>correcting the learner without impeding harmonious communication. </em>

In the example above, Nezzy is trying to say that the truck is going or moving. However, he cannot utter the correct language usage properly. The father then corrects him by stating <em>"Oh! Did you see the truck going?"</em> In this way, Nezzy will learn the correct way of describing the truck through his dad's response. <u>Such way of correcting Nezzy's error </u><u>doesn't obstruct the pattern of communication.</u>

So, this explains the answer.