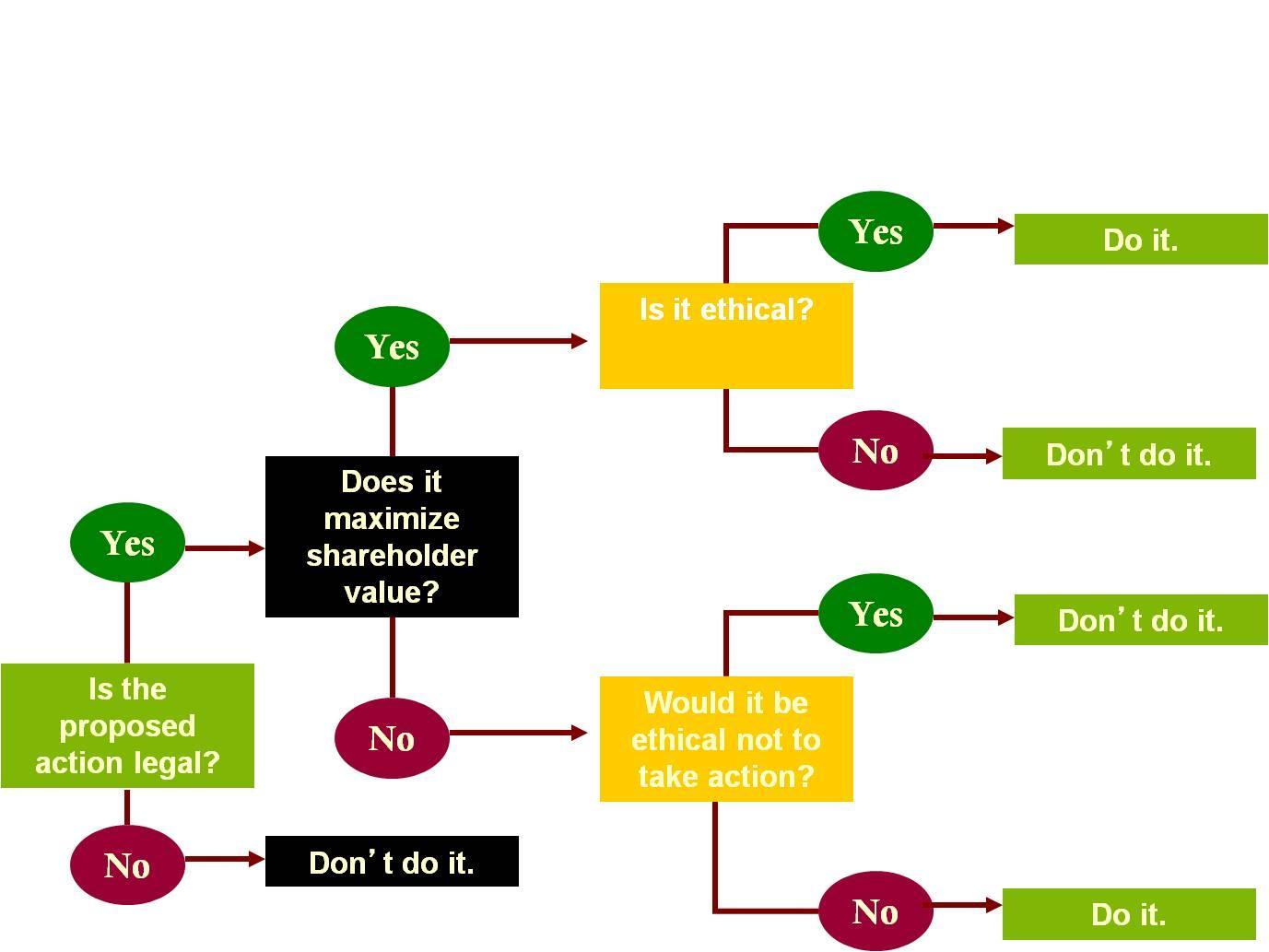

Answer:

Is the proposed action legal?

Explanation:

The very first step in the decision tree (below) was ignored. Disregarding local laws is ignoring the question of legality.

In the opening as the introduction is the place where introduce the problem, need, or opportunity that will address by the person, in a proposal.

<h3>What does it mean to

write a proposal?</h3>

A proposal is a document that, technically speaking, tries to persuade the reader to adopt a plan or project that is being provided. For their operations to be successful and to land new contracts, the majority of firms rely on persuasive proposal writing.

A person can observe that a proposal frequently contains the following: a brief explanation of the problem, the suggested solution, the costs involved, and the benefits.

Thus, In the opening as the introduction is the place.

For more details about write a proposal, click here:

brainly.com/question/1341280

#SPJ4

False it may be from the organization itself they might try rewarding the worker for example a company might take the workers to expensive workshops or to a trip as a type of reward or giving them a bonus to their salaries or a health insurance or a simple thing like involving them in a decision this may motivate the worker and make them feel part of the company <span />

Answer:

none of these describe the savings and loan crisis

Answer:

9.68%

Explanation:

Percent Return on Investment is calculated as Net Profit / Cost of Investment x 100

Net Profit= $46,620 (1,000 x $46.62 per share) + $950 (1,000 x $.95 per share) - $43,370 (1,000 x $43.37 per share) = $4,200

Cost of Investment= $43,370 (1,000 x $43.37 per share)

Percent Return on Investment= $4,200 / $43,370 x 100 = 9.68%