Answer:

Dividends are fixed ⇒ Debt

Preferred dividends are fixed much like the interest payments made on debt which makes this a characteristic of debt.

Usually have no specified maturity date ⇒ Equity

Equity does not have an expiration or maturity date and preferred shares share this same characteristic.

Cost of preferred stock.

The value of a Preferred stock is calculated by the formula:

Price = Dividend / Cost of preferred stock

97.95 = 11 / Cp

97.95 * Cp = 11

Cp = 11/ 97.95

= 11.23%

Answer:

b. inelastic

c. Yes - it decreased

Explanation:

Elasticitiy of demand measures the responsiveness of quantity demanded to changes in price.

Elasticity of demand = percentage change in quantity demanded/ percentage change in price

= -2/4 = -0.5

The absolute value is 0.5

If the absolute value of the coffiecnet of elasticity of demand is less than one, demand is inelastic.

Demand is inelastic if a change in price has no effect on quantity demanded .

We can tell that the quantity demanded fell because of the negative sign in front of the percentage change in quantity demanded.

I hope my answer helps you

I would see the process ends with the receipt of the goods. I used to work for a large open pit mine and go to the purchasers for buying materials for drilling etc and there would be first the requisition, then the purchaser would contact the seller or client and order the goods, then they would be purchased with the right account and finally received.

Answer:

d. reduce interest rates to shift aggregate demand right.

Explanation:

If the Federal Reserve supports the incumbent, they would want that she wins the election. In order to do so they may want to stimulate the economy.

To do so, they may reduce interest rates. This increases the opportunity cost of saving, and thus people instead of saving, will take their money out and spend it. Which in turns shifts the aggregate demand curve to the right.

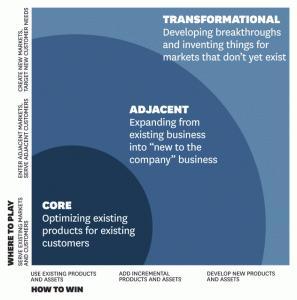

Answer:

Adjacent innovation

Explanation:

There are three ways to innovate in business:

1. Transformational

This is the most commonly thought of innovation. It has the potential to completely transform, create or eliminate entire industries. It involves one-in-a-million ideas that change the way the entire world lives and works.

This innovation is often seen as a means of disruption or a radical solution using breakthrough technology to achieve an unimaginable shift for markets that don’t exist yet.

2. Incremental

Incremental Innovation refers to the optimization of existing products for existing markets – ie. do what you’re doing but better: solving the current problems of your current clients, more effectively, sustainably and continuously.

It involves making smaller upgrades to existing products or services. The goal is to improve on existing products or services and renew interest in the marketplace.

3. Adjacent

Where Incremental innovation is all about improving existing products for existing markets, there are often opportunities to leverage an existing product, process, or infrastructure to reach new markets.

Simply put, adjacent innovation includes taking existing products into new markets and digital channels, or creating new digital products for existing markets. ie. Adjacent innovation involves entering a new market and connecting with a new audience by leveraging something the company already does well.