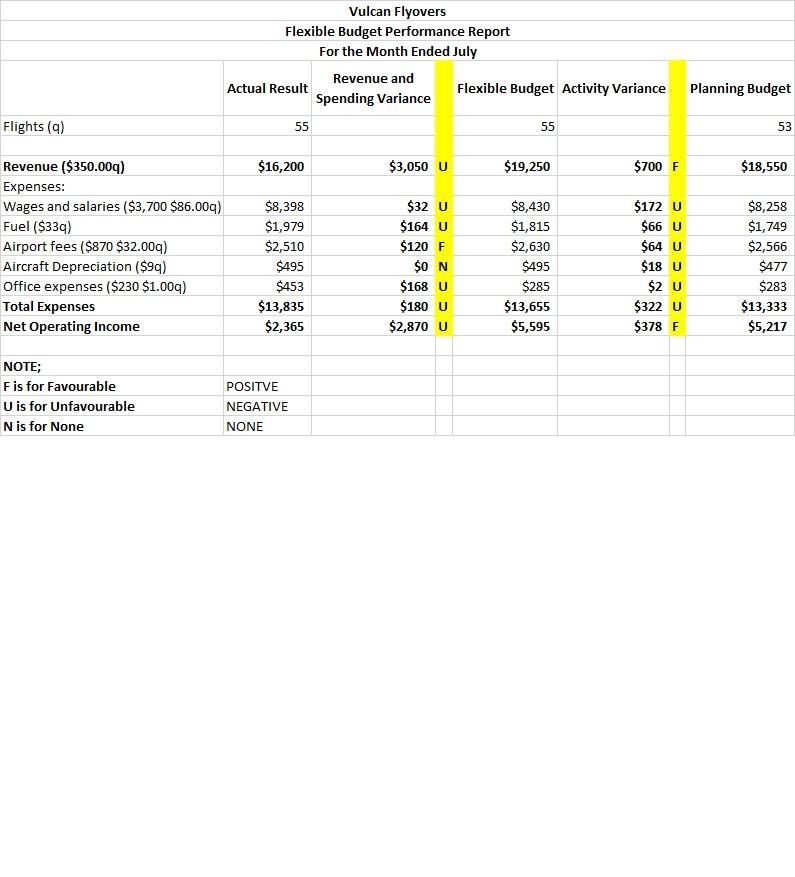

Answer:

Revenue and spending variance is Unfavourable

Activity variance is favourable

Explanation:

We need to determine Revenue and Spending Variance and Activity Variance.

Revenue and Spending Variance = difference between actual result and flexible budget. The above variance may be favourable or unfavorable or none

In the case of revenue, if the actual result figure is higher than the flexible budget, the revenue and expenditure variance is favorable and vice versa.

In case of expenses, if actual result figure is higher than flexible budget the revenue and spending variance is unfavorable and vice a versa.

F is for Favourable

U is for Unfavourable

N is for None

Activity Variance = difference between flexible budget and planning budget

. The above variance may be favourable or unfavorable or none

Actual Result Revenue and Spending Variance Flexible Budget Activity Variance Planning Budget

Flights (q) 55 55 53

Revenue ($350.00q) $16,200 $3,050 U $19,250 $700 F $18,550

Expenses:

Wages and salaries ($3,700 $86.00q) $8,398 $32 U $8,430 $172 U $8,258

Fuel ($33q) $1,979 $164 U $1,815 $66 U $1,749

Airport fees ($870 $32.00q) $2,510 $120 F $2,630 $64 U $2,566

Aircraft Depreciation ($9q) $495 $0 N $495 $18 U $477

Office expenses ($230 $1.00q) $453 $168 U $285 $2 U $283

Total Expenses $13,835 $180 U $13,655 $322 U $13,333

Net Operating Income $2,365 $2,870 U $5,595 $378 F $5,217

NOTE; Please see attached file.