deals with a microeconomic because it is the result of decisions that people and corporations make.

Describe "Microeconomics"

Microeconomics is the study of how people, households, and businesses make decisions and distribute resources. It mainly pertains to markets for products and services and addresses both personal and financial concerns.

The study of microeconomics focuses on the decisions people make, the factors that shape those decisions, and how those decisions have an impact on the supply, demand, and price of items on the market.

The probabilities (tendencies) that come from people making choices in response to shifting incentives, prices, resources, and/or production processes are the main subject of the study of microeconomics.

to know more about microeconomics

brainly.com/question/3539237

#SPJ4

You should always perform well and even better when no is around. respect and treat others as you would want to be treated.

Answer:

The correct answer is (D) business model

good luck

The answer to this question is an end-use segmentation. An

end-use segmentation is a marketing strategy which focuses on the way a

purchaser used the products. Marketing strategies are used to enhance / improve

the sales of product and services of the company.

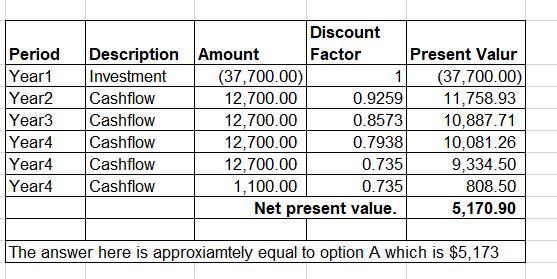

Answer:

Answer is (A) $5,173

Explanation:

In calculating the net present value of an investment we discount the future cash flows by multiplying the future cashflows by the discounting factors attached to each year the cashflows will arise.

See Attachment for calculation done.