Answer:

PV= $35,217,78

Explanation:

Giving the following information:

Future value= $2,500,000

Number of periods= 63 years

Interest rate= 7% compounded annually

<u>To calculate the value of the prize today, we need to use the following formula:</u>

PV= FV/(1+i)^n

PV= 2,500,000 / (1.07^63)

PV= $35,217,78

I think it is Carry a risk of losing money (A)

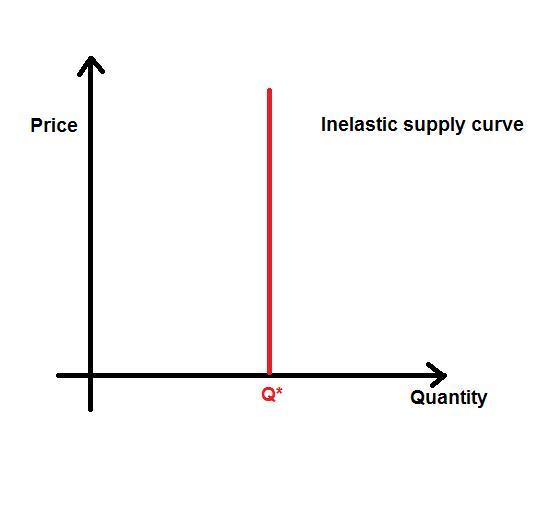

Answer: A perfectly inelastic supply curve means that<u><em> the quantity supplied is completely fixed.</em></u>

Perfectly inelastic supply states that supply is completely fixed. Therefore it is not affected by the change in price level.

<u><em>Therefore, the correct option in this case is (e)</em></u>

The management function that Shonda is performing when she decides that top managers will report to her while everyone else reports to the head of human resources is <u>iii. organizing.</u>

<h3>What is Organizing in management functions?</h3>

Organizing is that function of management involving the development an organizational structure so that human resources are arranged for the achievement of organizational objectives. Organizing also involves the design of the jobs of individuals.

Thus, the management function Shondra performs here is <u>Option III</u>.

Learn more about management functions at brainly.com/question/17083312

Answer:

Number of new shares:

= 100,000×(1÷2)

= 50,000

Amount of new investment:

= 50,000×$10

= $500,000

Total value of company after issue:

= $500,000+100,000×$40

= $4,500,000

Total number of shares after issue:

= 100,000+50,000

= 150,000

Share price after issue:

= $4,500,000÷150,000

= $30