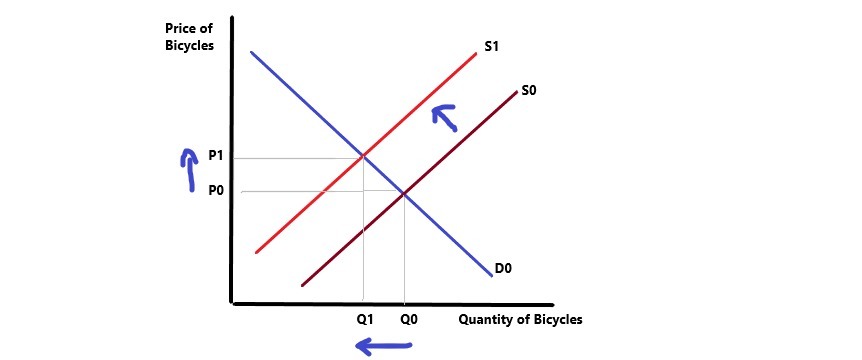

Answer: Higher price of bicycles

Explanation: Higher steel prices will lead to a rise in the input cost of the producers of bicycles. As a result of this, the supply for bicycles will decline shifting the supply curve upward to the left. With no information given about change in the demand for bicycles, the demand curve will not change.

The net effect will be an increase in the price of bicycles.

Answer:

To treat this in the bank reconciliation, the difference of $45 is deducted from the balance per bank.

Explanation:

Based on the information given;

The amount recorded (as a deduction) in the books was in excess of $45 being the difference between the actual amount $749 and the erroneous amount recorded $794.

As such, to reconcile the bank statement balance to the balance in the books, the difference $45 is deducted from the balance per bank.

However, in the computation of the book balance the excess amount $45 is added to the book balance to correct the error.

Answer: Price of cereals must fall by 12%

Explanation:

A 10% rise in the price of milk will lead to a fall in quantity demanded by =-0.9 * 10= 9%.

To prevent the demand for cereals from falling by 9%, the price of cereals must fall by

Thus, to offset the effect of a 10% rise in price of milk, the price of cereals must fall by 12%.

Answer:

product development

Explanation:

Product development growth strategy -

It is based on the modification of the existing product , so that they appear to be new and the development of the new products and then offering the product to the current or new market .

These types of strategy are adapted , when their is no scope of new opportunity foe the new company .

The strategy of product development is used in the question statement .