Answer:

ahem I love the world and my answer is 100% right ahem so dont report

Answer:

Prepare the necessary entry to clear the Intangible Assets account and to set up separate accounts for distinct types of intangibles.

- Dr Patents 387,900

- Cr Intangible assets 387,900

- Dr Goodwill 341,000

- Cr Intangible assets 341,000

- Dr Franchises 421,000

- Cr Intangible assets 421,000

- Dr Copyright 145,200

- Cr Intangible assets 145,200

- Dr Research and development expense 211,000

- Cr Intangible assets 211,000

Make the entry as of December 31, 2020, recording any necessary amortization:

- Dr Patents 387,900

- Cr Intangible assets 387,900

- Dr Amortization expense 43,100

- Cr Accumulated amortization - Patents 43,100

- Dr Goodwill 341,000

- Cr Intangible assets 341,000

- Dr Franchises 421,000

- Cr Intangible assets 421,000

- Dr Amortization expense 42,100

- Cr Accumulated amortization - Franchises 43,100

- Dr Copyright 145,200

- Cr Intangible assets 145,200

- Dr Amortization expense 29,040

- Cr Accumulated amortization - Copyright 29,040

*R&D costs are expenses, they are not amortized.

Reflect all balances accurately as of December 31, 2020. Use straight-line amortization

.

- Patents $344,800

- Goodwill $341,000

- Franchises $378,900

- Copyright $116,160

Answer:

A. Financial innovation motivated banks and other financial institutions to bypass the intent of the Glass-Steagall Act.

B. The Act's restrictions put American banks at a competitive disadvantage relative to foreign banks.

D. The Fed allowed bank holding companies to enter the underwriting business.

References for Explanation:

A. Financial Crisis Inquiry Commission. (2011). <em>The financial crisis inquiry report: The final report of the National Commission on the causes of the financial and economic crisis in the United States including dissenting views</em>. Cosimo, Inc. p. 21

B. Financial Crisis Inquiry Commission. (2011). <em>The financial crisis inquiry report: The final report of the National Commission on the causes of the financial and economic crisis in the United States including dissenting views</em>. Cosimo, Inc. p. 205

D. Financial Crisis Inquiry Commission. (2011). <em>The financial crisis inquiry report: The final report of the National Commission on the causes of the financial and economic crisis in the United States including dissenting views</em>. Cosimo, Inc. p. 300

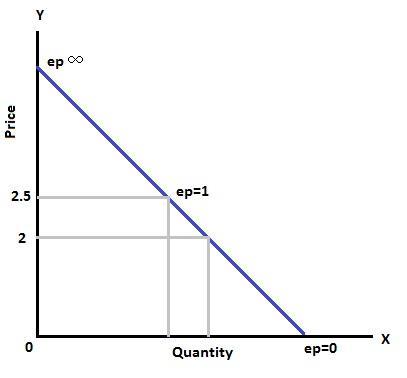

Answer:

The correct answer is option A.

Explanation:

The demand for cantaloupes is unitary elastic at price level $2.50. The demand curve here is linear and downward sloping. The elasticity of demand is 1.

In this linear demand curve the lower portion will represent inelastic demand.

When the price level is reduced to $2 the demand will move to the lower portion of the curve, with fall in price and increase in demand.

So, at $2 price the demand will be inelastic, which means it will be between 0 and 1.

Micheal’s Craft store is a public corporation. Because it acts as a single entity and its shares are traded freely on a stock exchange (it’s stocks can be freely viewed by anyone, not just the stock market privately)