Answer:

1. False.

2. False.

3. True.

4. False.

5. False.

6. True.

7. Computer support specialist.

8. True.

Explanation:

1. Employers generally restrict or monitor the Internet activity of their employees because the increased use raises the company's ISP rates significantly: False because it is considered unethical under certain employee rights.

2. Although unethical, there are currently no laws in the U.S. for actions such as hacking and sharing copyrighted material: False because there is a computer fraud and abuse act in existence.

3. Employees who engage in telecommuting may find themselves working more hours, especially if their supervisor feels as if they are always "on the clock.": True

4. Most experts recommend that companies monitor their employees secretly in order to prevent workers from circumventing the technologies used to track them: False because it is not ethical and violates the fundamental rights of the employees.

5. Copyright protection lasts 20 years after the date of publication or release: False because a copyright protection is 95 years from date of publication or release and 120 years from creation.

6. A web developer creates and maintains websites for organizations: True

7. A computer support specialist excels when it comes to installing, configuring, and supporting computer systems.

8. Creative works such as books, songs, and photographs are protected by copyright law: True

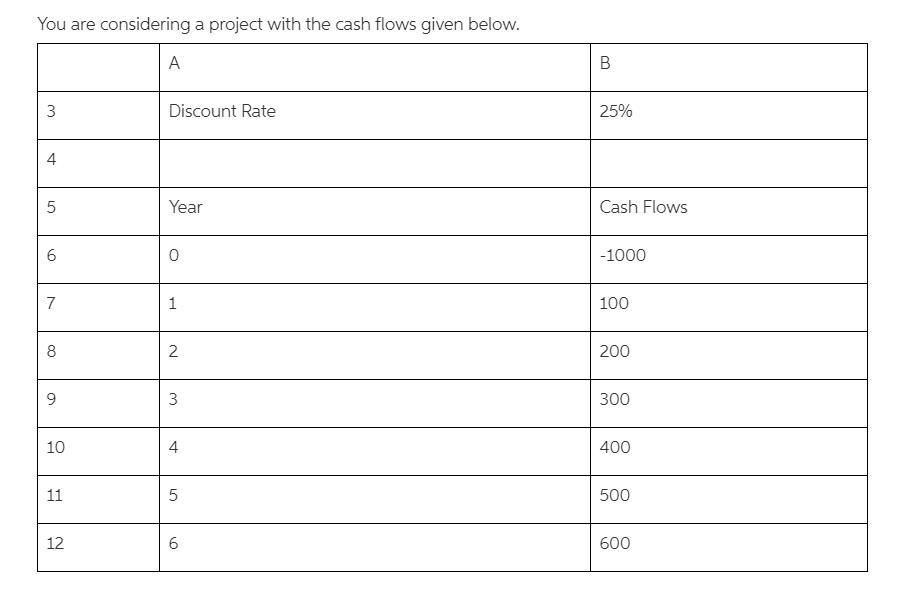

Answer:

$260

Explanation:

the cash flows associated to this project are:

year 0 = -$150

year 1 = $121

year 2 = -$242

year 3 = $665.50

the discount rate is 10%

using a financial calculator, the project's net present value (NPV) = $260

since the NPV is positive, then this project should be carried out

Answer:

Change in Net worth= $133.62

Explanation:

The two lease options require that the leasee ( the tenant) commit himself to pay a series of equal amount of rent installment at the different time period in the future.

These series of equal periodic cash flows occurring in the future are called annuities.

To have a meaningful comparison, the two annuities should be compared based on their present values. So we compute the present value of the two using the formula below:

Present Value (PV) =( A × (1- (1+r)^(-n))/r

Option 1:Current lease

PV = 500 × 1-(1+0.05)^(12)

= 500 × 8.863251636

= $4,431.62

Option 2: New Offer

This will be done in two steps:

PV of lease in year 3

PV =700 × (1-(1+0.05)^(-9))

= 700 × 7.107821676

=4,975.47

PV of lease in year 0

PV = FV × (1+r)^(-3)

=4,975.47 × 0.8638

=$4,298.00

My net worth would change by the amount of the difference between the two PV of the two annuities:

Difference in PV = $4,431.62-$4,298.00

Change in Net worth= $133.62

Answer:

A. Gretchen is incorrect because there is a binding bilateral contract.

Explanation:

Mainly there are two types of contract i.e unilateral contract and the bilateral contract.

The unilateral contract is the contract when the offer is made to the anyone

while the bilateral contract is the agreement in which the both parties are agreed and bind to perform his/ her obligations.

In the given case, it reflects the bilateral contract as the Haley returns the dog and he requested for the money from the Gretchen

Answer:

n = 100 customers

X = 80 who paid at the pump

A) the sample proportion = p = X / n = 80 / 100 = 0.8

we can definitely state that 80% of the customers paid at the pump.

B) if we want to determine the 95% confidence interval:

z (95%) = 1.96

confidence interval = p +/- z x √{[p(1 - p)] / n}

0.80 +/- 1.96 x √{[0.8(1 - 0.8)] / 100}

0.80 +/- 1.96 x √{(0.8 x 0.2) / 100}

0.80 +/- 1.96 x √{(0.8 x 0.2) / 100}

0.80 +/- 1.96 x 0.4

0.80 +/- 0.0784

confidence interval = (0.7216 ; 0.8784)

C) We can estimate with a 95% confidence that between 72.16% and 87.84% of the customers pay at the pump.