Answer:

Cost of goods manufactured= $3,120

COGS= $2,750

Explanation:

<u>To calculate the cost of goods manufactured, we need to use the following formula:</u>

cost of goods manufactured= beginning WIP + direct materials + direct labor + allocated manufacturing overhead - Ending WIP

Cost of goods manufactured:

beginning WIP= 0

direct materials= 2,200

Direct labor= 1,000

Factory overhead= 520

Ending work in process= 600

Cost of goods manufactured= $3,120

<u>Now, we can determine the cost of goods manufactured:</u>

COGS= beginning finished inventory + cost of goods manufactured - ending finished inventory

COGS= 0 + 3,120 - 370

COGS= $2,750

Answer:

The correct answer is: $60.

Explanation:

Opportunity Cost is what a person sacrifices when they choose one option over another. It is also defined as the revenue of the chosen option over the revenue of the option that was forgone. It represents what was left on the table for deciding taking one option over another.

In Ben's case, the opportunity cost of going to the event represents what he could have earned working for three hours (<em>$10 x 3 = $30</em>). However, as he will have to pay for the event, he will lose $30 for the event ticket. Then, the total opportunity cost of going to the event is:

$30 + $30 = $60

Answer:

$250,000

Explanation:

Since the purchase cost of an old equipment is already incurred and it does not have any kind of impact in decision making so this cost would be considered as the sunk cost i.e. $250,000

The operating cost of old & new equipment would be relevant for calculating the annual cost savings and the current selling value of the old equipment would also be relevant as salvage value

Therefore $250,000 would be considered

Answer:

Break-even point in composite units = 811 units

Explanation:

Number of modal;

5 Youth models

9 Adult models

6 Recreational models

Annual fixed costs total = $6,550,000

Find:

Break-even point in composite units

Computation:

Mixed contribution margin = 5[130] + 9[475] + 6[525]

Mixed contribution margin = 650 + 4275 + 3150

Mixed contribution margin = $8075

Break-even point in composite units = Annual fixed costs total / Mixed contribution margin

Break-even point in composite units = 6,550,000 / 8075

Break-even point in composite units = 811 units

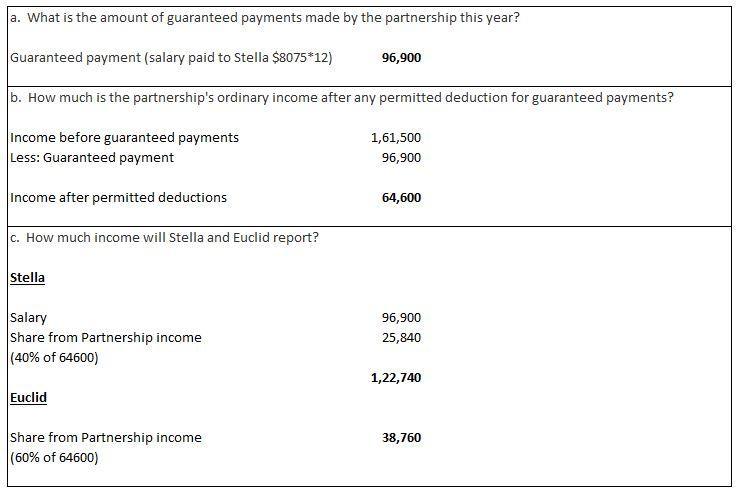

Answer

The answer and procedures of the exercise are attached in the image below.

Explanation

Please consider the data provided by the exercise. If you have any question please write me back. All the exercises are solved in a single sheet with the formulas indications.