Storage, retrieval is the correct answer

Answer:

Sales.

Explanation:

Pricing strategy can be defined as an approach utilized by different organizations to get the best price for a particular product or service.

Pricing strategy helps the organisation to create prices so as to maximise their profits. It could be influenced by factors such as latest economic trends, the demand of the consumers.

Sales orientation pricing strategy describes the different ways in which marketers persuade potential customers to purchase their products rather than understanding the different needs of their customers.

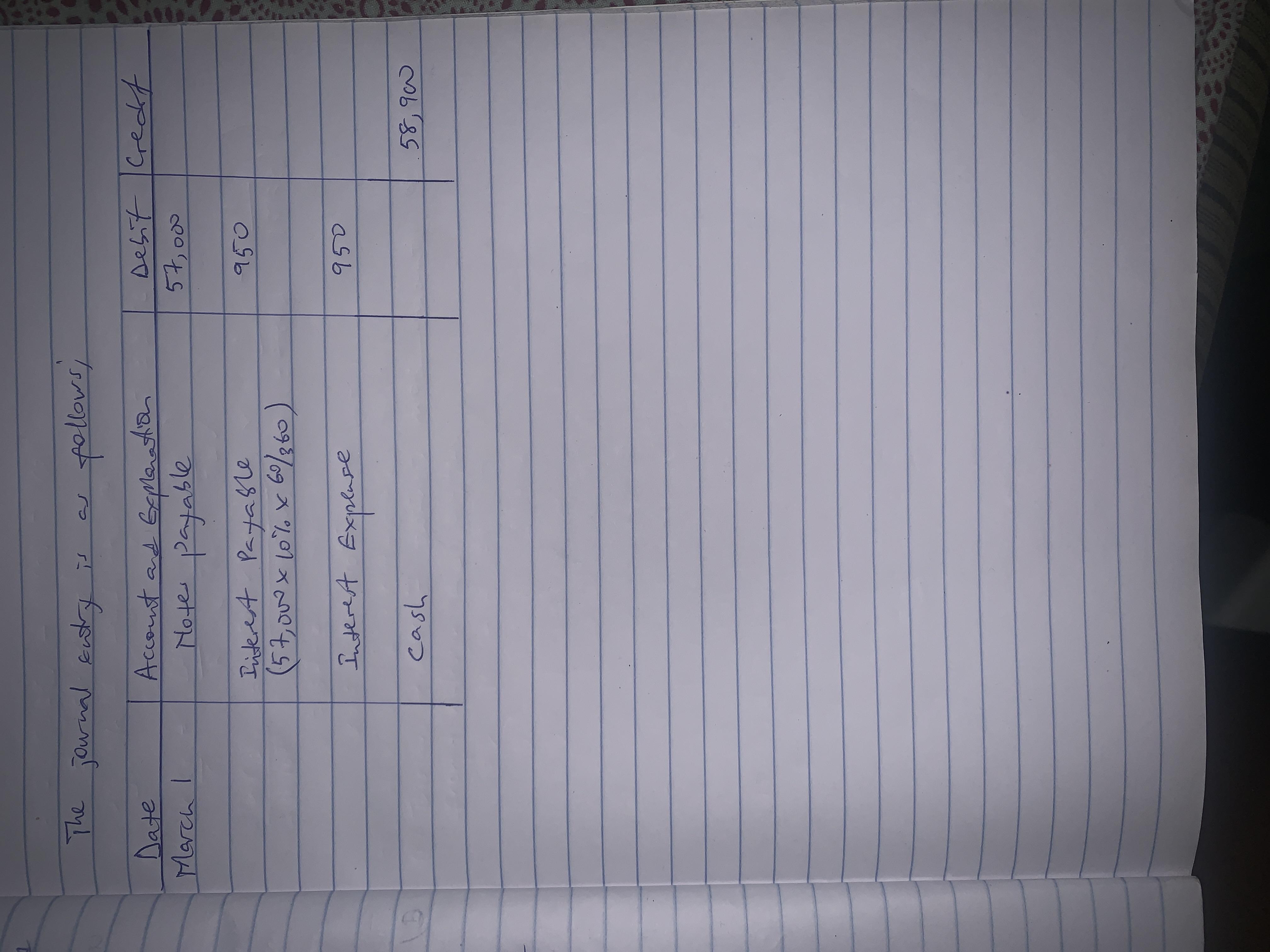

Answer:

Amount paid to record is $58,900

Explanation:

In this question, we are asked to state the Journal entry as of March 1.

Please check attachment for tabular explanation

Kindly note that 360 is used as the number of days in a year

Answer:

Current value per share is $13.33

Explanation:

The two stage growth model of DDM can be used to calculate the price of the share today. The DDM values a stock based on the present value of the expected future dividends from the stock. The price of this stock under this model can be calculated as follows,

P0 = D0 * (1+g1) / (1+r) + [ (D0 * (1+g1) * (1+g2) / (r - g2)) / (1+r) ]

Where,

- g1 is the initial growth rate which is 20%

- g2 is the constant growth rate which is 5%

- r is the required rate of return

P0 = 1 * (1+0.2) / (1+0.14) + [ (1 * (1+0.2) * (1+0.05) / (0.14 - 0.05)) / (1+0.14) ]

P0 = $13.33

Answer:consumers

Explanation:

In a free-market system, consumers and producers have sovereignties that drive the market and decisions made to ensure that supply and demand