I would say it would deal with one's humanity to man to decide who to rescue with only three seats to fill in other words, the best choice would be to rescue the elderly and/or women with babies or small children, or the sick to help those most in need.

Answer:

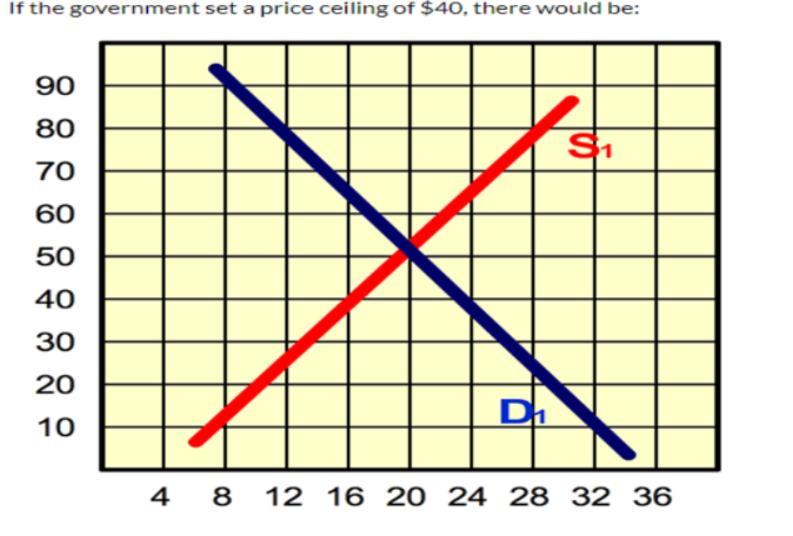

A surplus (or excess demand) of about 8 units

Explanation:

The picture attached shows the diagram necessary for the question which is part of the question. Solution is given below;

At the above ceiling at price of 40$

Quantity supplied will be 16

Quantity demanded will be 24

So when demand is more than supply than there will be a shortage in quantity by (24-16) 8 units.

When there is demand more than supply than it is an excess demand.

So surplus or excess demand by 8 units.

Answer:

c. Psychological

Explanation:

Maslow's heirachy of needs states that people are driven to find a job or a means of livelihood because of various motivation factors. These needs must be satisfied before a person looks to obtain other less important needs.

The first level of needs are the psychological needs. These have to be satisfied before an employee will look to other needs.

They include man's basic needs to live like food, shelter, and clothing.

After these are satisfied one can now focused on security needs, social needs, esteem needs, and self actualization.

Answer:

verbal expression - the communication (in speech or writing) of your beliefs or opinions; "expressions of good will"; "he helped me find verbal expression for my ideas"; "the idea was immediate but the verbalism took hours"

expressão verbal - a comunicação (oral ou escrita) de suas crenças ou opiniões; “expressões de boa vontade”; "ele me ajudou a encontrar expressão verbal para minhas idéias"; "a ideia foi imediata mas o verbalismo demorou horas"

Explanation:

brainliest please?

coroa please?

Answer:

Private savings has decreased.

Explanation:

The crowding out effect occurs when government intervention in the economy reduces either private investment or saving.

In the case of saving, this can occur if the government crowds out private investment by taking up large loans that cover most of the market for loanable funds. This will in turn reduce the incentive or capacity of private investors to save, reducing private saving, and decreasing the supply of loanable funds, causing the shift in the curve.