Answer:

Option (c) is correct.

Explanation:

Net cash provided by operating activities:

= Net income + Depreciation + loss on sale of Equipment + Decrease in prepaid expense + Increase in account payable - Increase in account receivable - increase in inventory - Decrease in accrued expenses

= $132,000 + 44,000 + 8,000 + 60,000 + 52,000 - 60,000 - 100,000 - 24,000

= $112,000

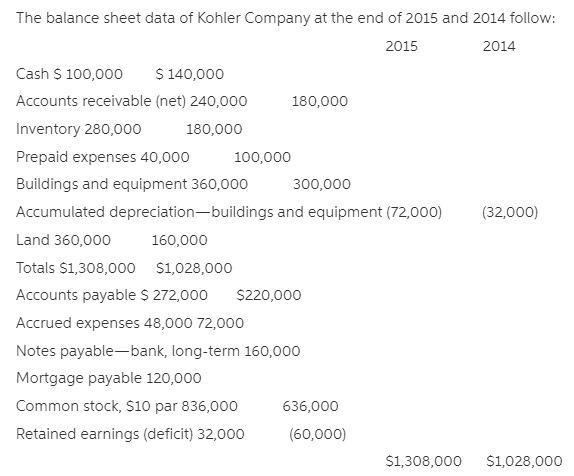

Note:

The balance sheet is missing in this question, so I attached the balance sheet with the answer.

Answer:

$248,000

Explanation:

Given that 20% of sales are for cash, Of the credit sales, 10% are collected during the month of sale, 30% in the following month, and 60% in the second following month. It means that credit sales is 80% of sales.

Cash collection for January will include 20% sales in January, 8% (10% * 80%) sales in January, 24% (30% *80%) sale in December and 48% (60% * 80%) of sales in November.

The forecasted amount of total CASH COLLECTIONS FROM SALES in January

= 20% * $200,000 + 8% * $200,000 + 24% * $400,000 + 48% * $200,000

= $40,000 + $16,000 + $96,000 + $96,000

= $248,000

<span>A good rule is that you will sno more than 25 - 30% of your gross income. You ought to spend close to 30 percent of your pay on lodging. You may hear that dependable guideline from a monetary counselor or parent, a landowner or bank. It's implanted in online spending adding machines and government approaches. The standard business proposal for contract installments is that close to 30 percent of your gross salary ought to go to your regularly scheduled installments.</span>

Answer:

The depreciation cost of the bus per unit is $ 1.4 which is purchased on January 1, 2019.

Explanation:

The depreciation cost per unit is computed as:

Depreciable asset = Cost - Salvage Value

= $205,860 - $7,900

= $197,960

Depreciation per unit = Depreciable asset /Useful life expected value

= $197,960 / 141,400

= $1.4

Therefore, the per unit cost is $1.4

Answer:

d. explicit forecast period and a terminal value

Explanation:

The concept involves giving the current values to the expected future cash flows of a project. Discounted cash flows seek to assign a present value to the projected future income of a company. The discount cash flow techniques use an appropriate discount rate in evaluating forecasted revenues.

Discounted cash flow valuation methods are used in capital budgeting. They are decision-making tools that help managers and shareholders determine whether to invest in a project or not. Discounted future revenues communicate the profitability potential of a project.