Answer:

The correct answer is option c.

Explanation:

Game theory is a tool in economics. It helps to understand the situation in cases where rational players interact and act in a strategic manner. For instance in an oligopoly market where there are few firms, which are interdependent.

These firms or producers are rational players who have to decide output and price level in order to maximize their economic profits.

The theory of monopoly can be applied only in case of monopoly market. The cartel theory is applicable if firms have formed a cartel. Aggressive competition model is not always necessary.

So, the correct answer here will be option c.

Answer:

Spillover cost.

Explanation:

Spillover cost refers to those costs or changes in the value of a certain good that are caused by issues external to the intrinsic characteristics of said good. Thus, for example, external influences such as limitations on oil extraction or the development of electric cars can generate a massive drop in the prices of conventional gasoline cars. Another clear example of this situation is the one described in the question, where a negative change in a certain neighborhood can lower the prices of the houses found there.

This question seems incomplete. Here is the detailed and complete question:

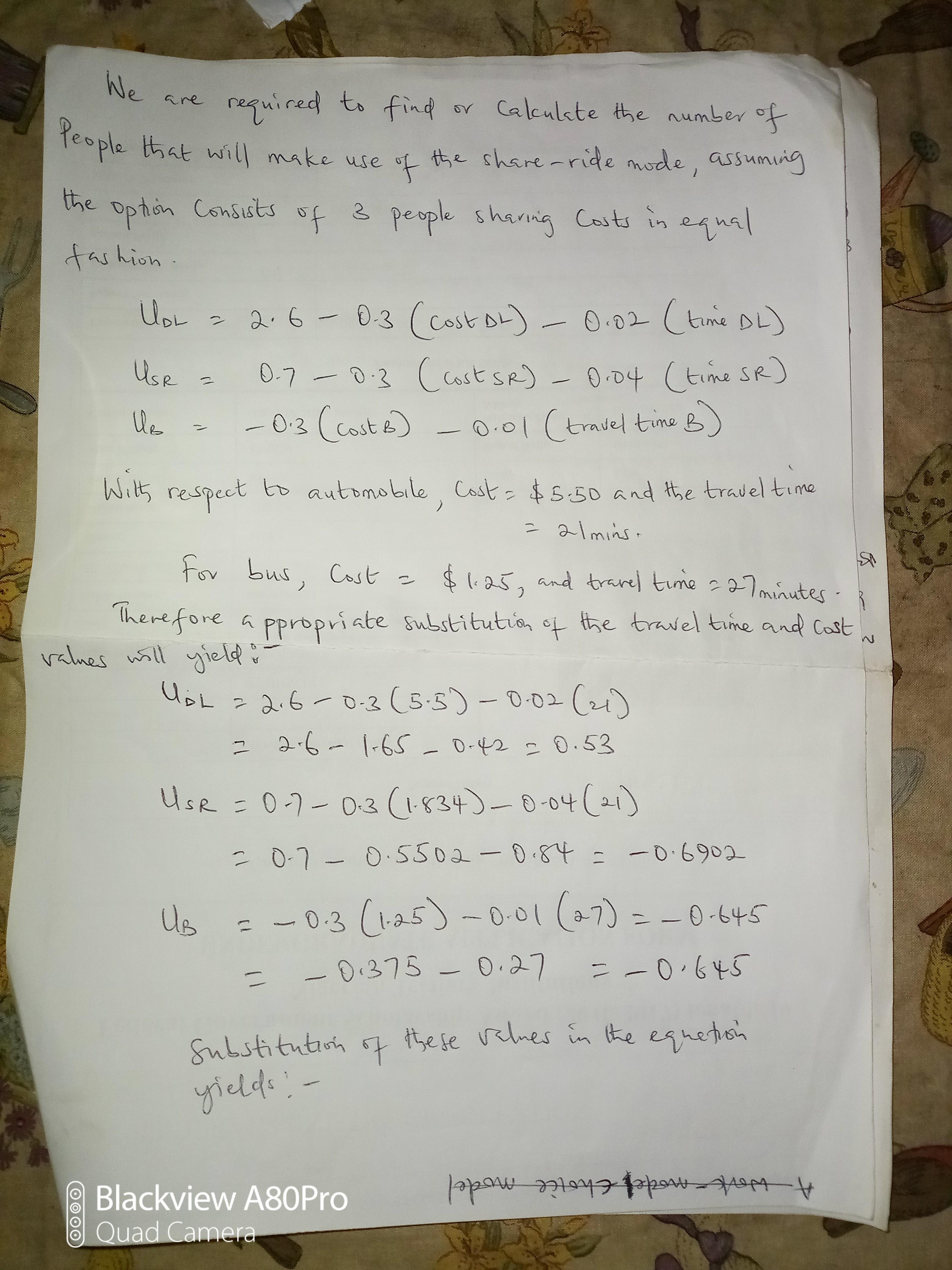

A work-mode-choice model is developed from data acquired in the field in order to determine the probabilities of individual travelers selecting various modes. the mode choices include automobile drive-alone (dl), automobile shared-ride (sr), and bus (b). the utility functions are estimated as follows: udl = 2.6 - 0.3(costdl) - 0.02(travel timedl) usr = 0.7 - 0.3(costsr) - 0.04(travel timesr) ub = -0.3(costb) - 0.01(travel timeb) where cost is in dollars and time is in minutes. the cost of driving an automobile is $5.50 with a travel time of 21 minutes, while the bus fare is $1.25 with a travel time of 27 minutes. how many people will use the shared-ride mode from a community of 4500 workers, assuming the shared-ride option always consists of three individuals sharing costs equally?

Answer: 828 workers will use the shared - ride mode.

Explanation: You can see the attached for a more detailed explanation.

Here are some hard math questions for 4th graders:

1. 6/2(1+2) = ?

2. (Word Problem)

Linda read 60 minutes for each day for 6 days. Teala read 55 minutes each day for 7 days. What is the difference, in minutes, between the total amount of time Linda read and the total amount of time Teala read.

(((The second question is a common core 4th grade question.

Given: Variable Cost Fixed Cost

per haircut per month

base salary 9660

manager bonus 530

commission 5.92

advertising 270

rent 940

barber supplies 0.30

utilities 0.25 180

magazines 25

Total 6.47 11605

Revenue 11.47

Break even point in unit = Fixed expenses per month / Contribution margin per month.

Break even point in unit = 11,605 / (11.47-6.47) = 11,605 / 5 = 2,321 haircuts

Break even point in $ = Fixed expenses / Contribution margin ratio

Break even point in $ = 11,605 / (5/11.47) = 11,605 / 0.44 = 26,375

Net Income = (Contribution Margin * # of haircuts) - Fixed expenses

Net Income = (5 * 2,380) - 11,605 = 11,900 - 11,605 = 295