Answer:

HRA

Explanation:

HRA is health reimbursement accounts (or Health Reimbursement Arrangement). This is a type of employer-funded benefit that reimburse for medical expenses of employees in specific types of cases. Money in this account can be carried at the end of the current to the next year.

So that in the case of Jenna, her current corporate company is the one funding the account. So that, the money would lose when Jenna switches to another job.

A consequence of paying most or all of a salesperson's compensation in the form of commissions is It encourages the salesperson to focus on closing the sale.

A sales commission is a payment made to an employee after they successfully complete a task, typically selling a predetermined volume of goods or services. Sales commissions are a common incentive used by employers to boost employee productivity. A commission can be paid instead of or in addition to a salary.

A commission is a fee a broker or investment advisor charges for handling a client's purchases and sells of securities or for offering financial advice.

Learn more about commissions here

brainly.com/question/20987196

#SPJ4

Answer:

refine your approach by going back to the drawing board

Explanation:

Considering the scenario described above in the question, the best thing to do is "refine your approach by going back to the drawing board."

This will give you the chance and opportunity to look for a better plan, then find a perfect segmentation approach that really meets and satisfy all of the effective segmentation conditions.

Answer: Debit Unearned fees $6,120, Credit Fees income $6,120.

Explanation: Garcia Publishing received $24,480 from Otisco on April 1 and this was recorded as unearned fees. This means Garcia would have debited cash with $24,480 and credited unearned fees $24,480. Remember the fees was paid at the beginning of April and is for 36-month subscriptions. So, the amount in unearned fees would be unwound to income (fees) over the tenor of the subscription (36 months). Therefore, monthly amortization would be $24,480 divided by 36 months = $680. April 1 to December 31 is 9 months, $680 multiplied by 9 months is $6,120.

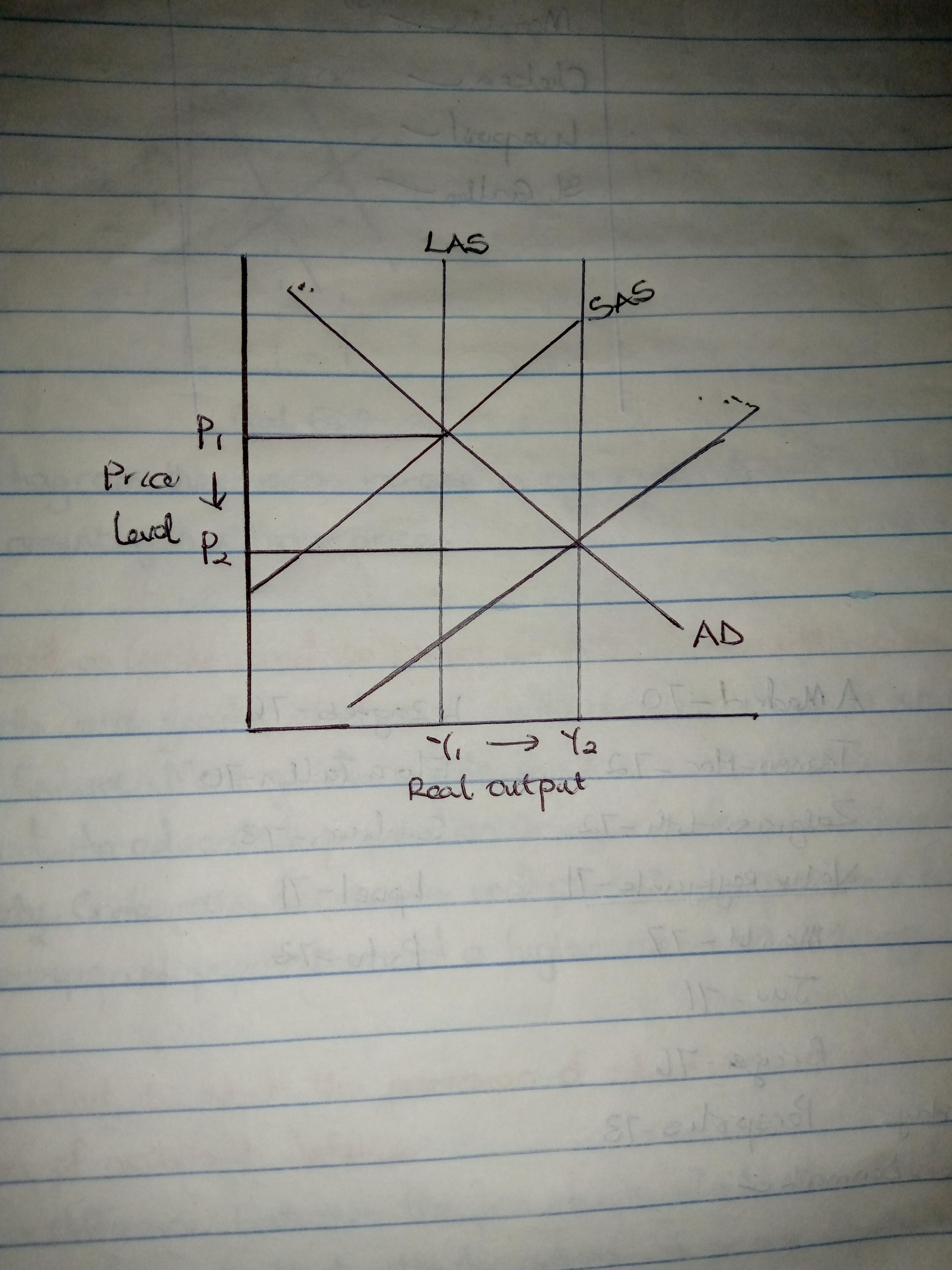

Answer: The price level falls and output rises.

Explanation:

According to Moore's law, it is stated that the computing speed of a microchip doubles every 18 months. According to Moore, this will increase thespeed and capability of computers and also bring about lesser pay for the computers.

The effect of this on the economy is that it will lead to a fall in price level and increase in output as there will be faster and cheaper production. This can be shown in the diagram attached.