Answer:

74 units and 90 units.

Explanation:

So, we have the demand for the first six months, K1 = 600 units = 600 units/ 6months = 100 units; the demand for the second six months, K2 = 900 units = 900/6 = 150 units; holding cost,J = $2 per unit ; process cost, P = $55 per order.

The formula for determining an order size that will minimize the sum of ordering and carrying costs for each of the six-month periods is the Economic Order Quantity formula which is given below;

Economic Order Quantity = √[ (2 × K1 × P)/ J ].

(1). For the first six months;

Economic Order Quantity = √ [ ( 2 × 100 × 55)/ 2].

Economic Order Quantity = 74 units.

(2). For the second six months.

Economic Order Quantity = √ [ ( 2 × 150 × 55)/ 2].

Economic Order Quantity = 90 units.

Answer:

28.57%

Explanation:

currently total shares outstanding are:

- you own 3 million shares

- angel investors own 2 million shares

- total shares outstanding 5 million

if the corporation issues 2 million shares more, then the total shares outstanding would increase to 7 million.

The venture capitalist's investment in your firm would represent 2/7 = 28.57% of the firm's total shares.

Answer:

<u>Price</u> risk is the risk of a decline in a bond's value due to an increase in interest rates. This risk is higher on bonds that have long maturities than on bonds that will mature in the near future.

<u>Reinvestment</u> risk is the risk that a decline in interest rates will lead to a decline in income from a bond portfolio. This risk is obviously high on callable bonds. It is also high on short-term bonds because the shorter the bond's maturity, the fewer the years before the relatively high old-coupon bonds will be replaced with new low-coupon issues.

Which type of risk is more relevant to an investor depends on the investor's <u>investment horizon</u>, which is the period of time an investor plans to hold a particular investment.

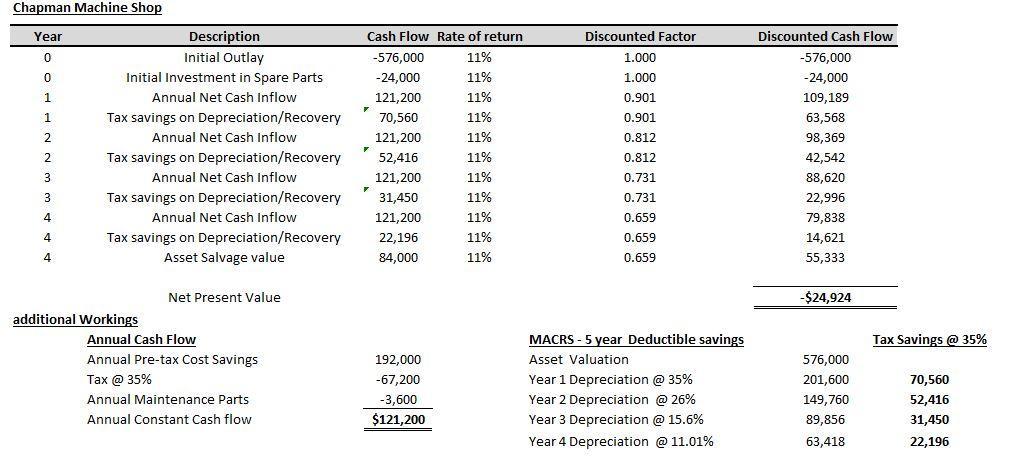

Answer:

The Firm should not Buy and Install the press as it delivers a negative NPV of -$24,924 at 11% discount rate over its 4 year operations

Explanation:

The General rule is to appraise the investment based on various appraisal techniques.

A technique that should be considered must have special focus on the time value of money, the required rate of returns expected by the firm and other Cashflow considerations.

The Net Present Value (NPV) approach will be the best method to proceed with.

The NPV approach typically falls under the following decision tree:

a. If NPV is negative (Reject the proposal)

b. If NPV is positive (Accept if it's a singular project, Accept the highest positive NPV if it's for mutually exclusive Projects)

c. If Zero (this is the breakeven line at which the Project covers all its cost but does not return a profit.) Also referred to as the IRR

Kindly refer to the attached for detailed workings