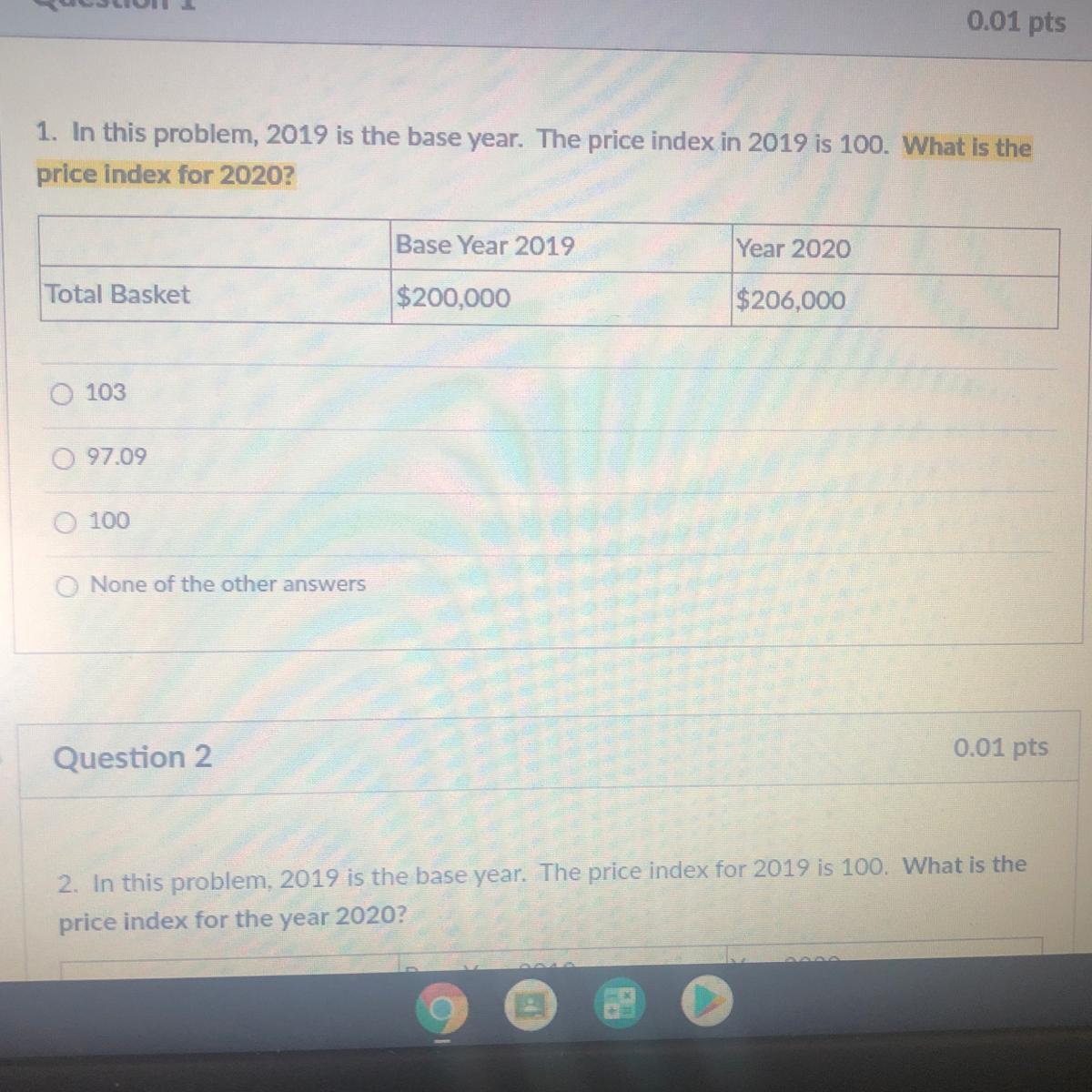

Answer:

r = 0.139 or 13.9%

Option e is the correct answer

Explanation:

Using the CAPM, we can calculate the required/expected rate of return on a stock. This is the minimum return required by the investors to invest in a stock based on its systematic risk, the market's risk premium and the risk free rate.

The formula for required rate of return under CAPM is,

r = rRF + Beta * (rM - rRF)

Where,

- rRF is the risk free rate

r = 0.04 + 0.9 * (0.15 - 0.04)

r = 0.139 or 13.9%

The answer is A. ^^ hope that helps!

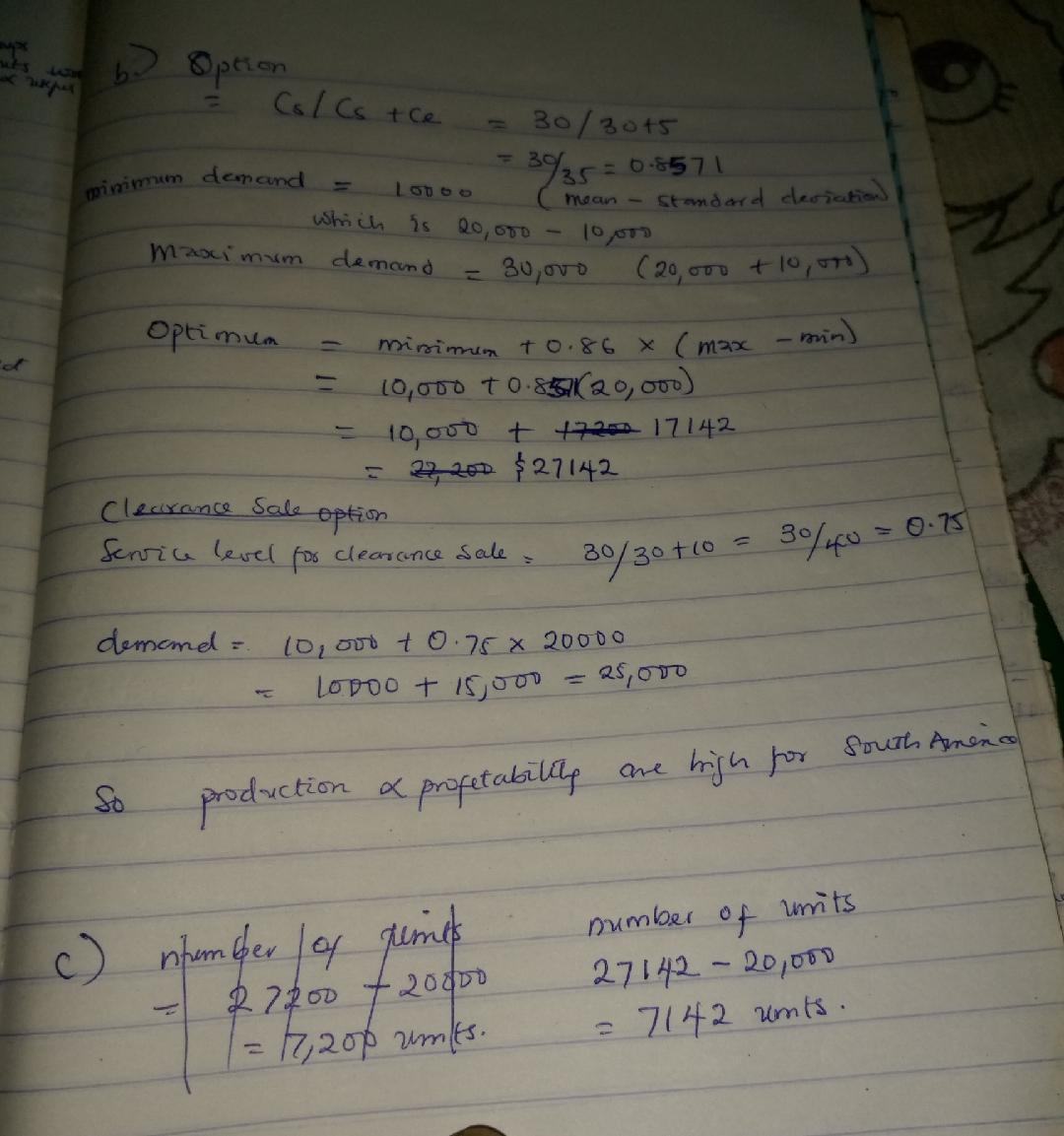

Answer:

The question puts

Mean demand to be 20000

Standard deviation to be 10000

Storage cost = 60-30= 30

Excess cost to be 30+5-25 = 10

For shipping to south america

Excess cost = 30+5+5-35 = 5 dollars

A.

It is of more benefits to ship to south america because we have an excess cost of 5 dollars and excess clearance cost of 10 dollars

B.

Production and profitability are high for south america. Please check attachment for the calculations I added

C.

Number of units

27142-20000

= 7142 units.

Answer:

I dont know the answer but I want whatever job she has

Answer:

$131.58

Explanation:

The computation of the new stock price is shown below:

= Selling price of stock per share ÷ current number of shares

= $250 ÷ 1.90

= $131.58

Since the 90% dividend is declared. It means for each share 90% dividend is declared so after stock dividend, the number of shares would be

= 1 + 90%

= 1 + 0.9

= 1.9

We simply divide the selling price by the current number of shares