Answer:

The number of adult tickets is 371.

The number of children's tickets is 629

Explanation:

Let A be the number of adult tickets sold and C be the number of children's tickets sold. The following linear system can be modeled based on the information provided:

Solving the linear system:

The number of adult tickets is 371.

The number of children's tickets is 629.

Answer:

The answer to this question can be defined as follows:

Explanation:

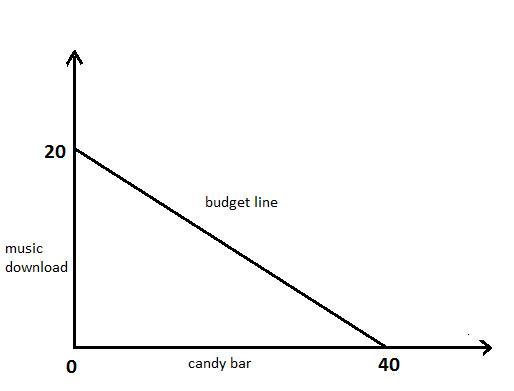

Please find the graph in attachment.

In point a.

The candy bar price

In point b.

The music download price

In point c.

The opportunity cost for music download

In point d.

The opportunity cost for a candy bar

In point e.

The cost of opportunity won't change as the price of the items is constant.

Answer:

Variable costs per hair cut: =$12

Total fixed costs: =$12,840

Explanation:

Variable costs are the cost that changes depending on the output level. For this barbers shop, variable costs are

Barbers commission= $11.40

Barber supplies: $0.45

supplies $0.15

Total variable cost per hair cut

= $11.40 + $0.45 + $0.15

=$12

Fixed costs will be the constant costs throughout the year. They will be the same months after month.

Fixed costs for the barber shop will be

Base rate : $1570 x 7 =$10,990

Managers extra pay = $525

Advertising = $240

Rent $900

Utilities $150

Magazines $35

Total fixed cost

=$10,990 + $525, + $240, + $900, + $150, + $35

=$12,840

Answer:

The answer is: D) Risk is a measure of the uncertainty surrounding the return that an investment will earn.

Explanation:

Investment risk refers to the probability of losing an investment. It measures the uncertainty level of earning returns from an investment.

When an investor anticipates a higher risk, he will expect higher returns. On the contrary, low risk investments (e.g. T-Bills) offer very low yields.

Answer:

The correct answer is letter "C": is a plan for a single level of activity, whereas a flexible budget adjusts for changes in the activity level.

Explanation:

Budget variance can be measured by using a static budget or a flexible budget. Both measures must be done at the end of an accounting period. A static budget is forecasted at the end of a year and reflects the changes in costs -mainly raw materials- of the operations of business throughout the period. They are prepared for one level of production volume only and do not change after developed.

Flexible budgets are estimated by the beginning of the period by can change during the year according to the production level. They are estimated for different levels of volume and separate fixed and variable costs.