When she altered her shopping patterns and buying behavior because of substantial pay raise, it is an example of income effect.

In economics, Income effect explains how their is a <u>change in demand</u> in market caused by of a change in <u>consumer's purchasing power</u> as a result of a <u>change in their real income</u>.

Here, the theory of <u>income effect</u> explains Gall's situation because her increase in pay cut changes her purchasing power, thus, increases her demand for expensive goods.

In conclusion, when she altered her shopping patterns and buying behavior because of substantial pay raise, it is an example of income effect.

Read more about this here

<em>brainly.com/question/22093268</em>

Answer: An increase in government spending

Explanation:

Currency appreciation is an increase in the worth of one currency against the value of another currency. Due to the appreciation of a currency, imports get cheaper.

In a small open economy, the appreciation of the real exchange rate can be caused by an increase in government spending as this puts pressure on domestic currency to appreciate, which leads to current account deterioration.

On even-numbered years, the representative reelection happens. Thus a representative seeking re-election will not receive anything from the government. Only when the representative on the 2year active term will they receive the monthly compensation stipulated by the law which is $7,200 per month excluding per diem.

The primary output of operational design is the operational

approach that is being described in the operational environment as the problem

and as well as the commander’s visualization by which is in a broad approach

that is for the sake of achieving the end state that is being desired.

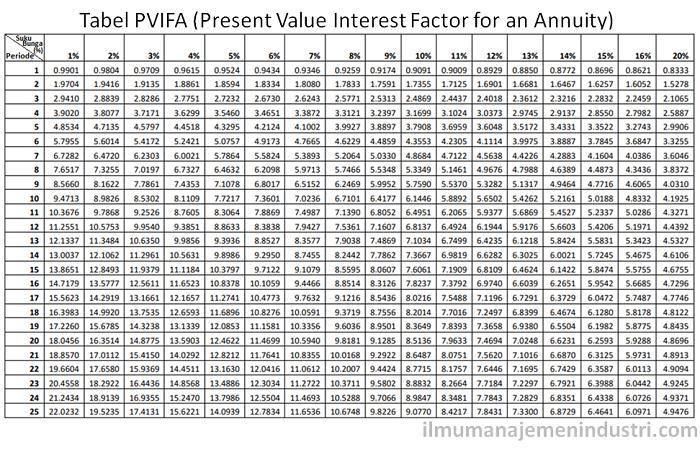

Answer: $70,882.98

Explanation:

Present value of note = Present value of interest payments + Present value of face value

Present value of interest payment:

First calculate the interest:

= 5% * 74,000

= $3,700

This amount is constant so is an annuity

Present value = 3,700 * Present value interest factor of annuity, 5 years, 6%

= 3,700 * 4.2124

= $15,585.88

Present value of face value :

= 74,000 / (1 + 6%)⁵

= $55,297.10

Present value of note:

= 15,585.88 + 55,297.10

= $70,882.98