Answer:

In a perfectly competitive industry the market price is also the marginal revenue of a firm and in order to maximize profit a firm has to produce a output at which marginal revenue is equal to marginal cost. In this case the firm's marginal revenue is fixed at 12 so they need to bring their marginal cost down to 12 in order to maximize profits. What they should do is decrease their output to a quantity so that their marginal cost is also 12, when they do this their marginal cost and marginal revenue will be equal and they will be maximizing profits.

Explanation:

Answer:

The options for this question are the following:

a. an exchange rate

b. a quota

c. a boycott

d. a dumping law

e. a tariff`

The correct answer is b. a quota

.

Explanation:

Import quotas are tools that countries have when it comes to limiting the physical quantity of a product that can be imported into their territories.

Within the different methods of control of foreign trade that a State has, there is the adoption of import quotas.

Therefore, this economic mechanism of trade restriction therefore supposes the application of limits of units or maximum weight of product that it is possible to import during a determined period of time.

Introducing this type of commercial measures is perfectly compatible with the introduction of others simultaneously. That is, a government can establish quota-based import trade strategies and set tariffs, for example.

The company's cost of good sold is $350,000. The cost of good sold is a cost which directly attributed to the inventory sold by a company. Gross profit is a portion of income which created by the selling of inventory ignoring other expense besides the cost of good sold. From the company's data, we can find the cost of good sold by finding the difference between net sales and gross profit, therefore the formula we have to use is "Cost of good sold = Net sales - gross profit".

Answer:

Explanation:

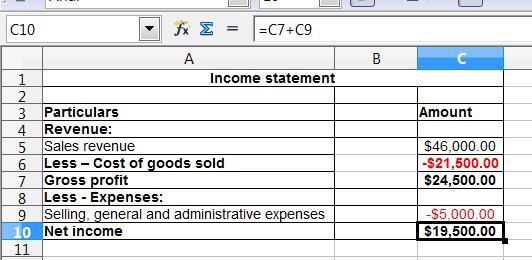

(a) The computation of the cost of goods sold is shown below:

= Beginning inventory + Purchase of new merchandise - ending inventory

= $4,000 + $22,000 - $4,500

= $21,500

(b) In the income statement, the total revenues and the total expenses are recorded.

If the total revenues are more than the total expenditure then the company earns net income

And, If the total revenues are less than the total expenditure then the company have a net loss

This net income or net loss would reflect in the statement of the retained earning account.

The preparation of the income statement is presented in the spreadsheet. Kindly find the attachment below:

Answer:

The first option is correct

Explanation:

So as to have a justifiable reason to issue a management report on internal control, based on Section 404(a) from the Sarbanes-Oxley Act of 2002, the following responsibilities are required from the Management:

• Create and maintain adequate internal control over financial reporting for the company

• Provide criteria for evaluators to assess the effectiveness of the company’s internal control over financial reporting

• Assess the effectiveness of the company’s internal control over financial reporting based on management’s evaluation of it, at year-end (i.e., a point-in-time assessment), including disclosure of any material weakness in the company’s internal control over financial reporting identified by management.

Therefore, to have a justifiable reason to issue a management report on internal control under Section 404(a) of the Sarbanes-Oxley Act of 2002, management must do everything, except "Establishing a system of internal controls containing no material weakness" as this was not stated under Section 404(a) of the Sarbanes-Oxley Act of 2002.

Hence first option is correct.