An increase in cash would definitely placed in debit because it considered an asset and we need to place the increase of sales on the credit side.

So, in this case, the entry would be

Cash $ 30,250

Sales $ 30.250

All leveling techniques delay by noncritical activities to reduce peak demand is known as resource smoothing.

If resources are sufficient but the demand differs extensively over the journey of the project, it may be sensible to smash resource demand by delaying noncritical activities to lessen peak demand and, in this way increase resource fulfillment. This process is called resource smoothing.

Resource smoothing is one of the project management devices used in the resource development techniques. It is interpreted as a technique that alters the activities of a scheme model so that all necessity for the resources do not excel the resource limits which is already pre-interpreted while planning. It is used when the time limitations takes important place in project planning.

To learn more about resource smoothing here

brainly.com/question/28259171

#SPJ4

Answer:

Answer for the question:

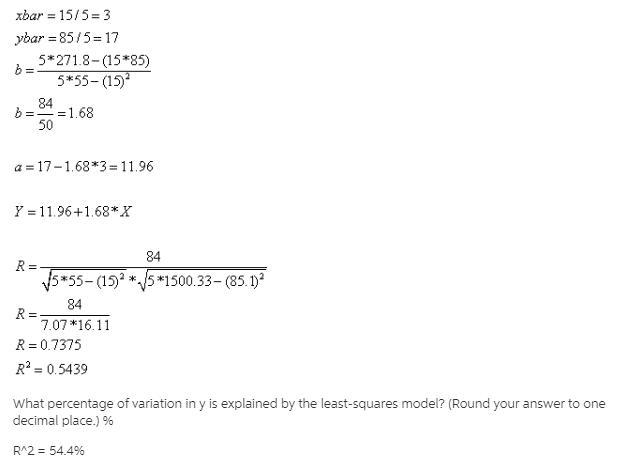

Bighorn sheep are beautiful wild animals found throughout the western United States. Let x be the age of a bighorn sheep (in years), and let y be the mortality rate (percent that die) for this age group. For example, x = 1, y = 14 means that 14% of the bighorn sheep between 1 and 2 years old died. A random sample of Arizona bighorn sheep gave the following information:x 1 2 3 4 5y 14 18.9 14.4 19.6 20.0 (a) Draw a scatter diagram. (3 points)(b) Find the equation of the least-squares line, and plot the line on the scatter diagram of part (a). (3 points)(c) Find the correlation coefficient r. Find the coefficient of determination . What percentage of variation in y is explained by the variation in x and the least squares model? (4 points)

is given in the attachment.

Explanation:

Answer:

Explanation:

In order to find the highest amount david can pay or in other words the present value of the investment we would have to discount the cash flows

3000/1.08+3000/1.08^2+3000/1.08^3+3000/1.08^4+3000/1.08^5=11,978

It seems that you have missed the necessary options for us to answer this question, so I had to look for it. Anyway, here is the answer. Unlike the marketing research problem, the management decision problem <span>focuses on problems that are much broader in scope. Hope this answers your question.</span>