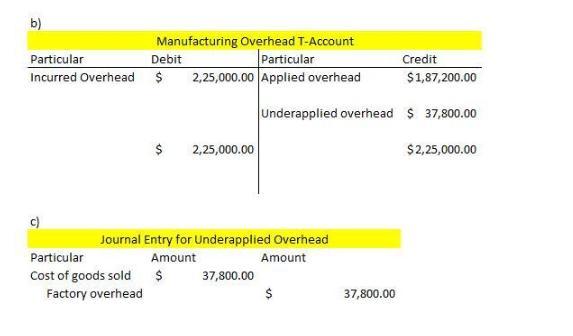

The underapplied overhead is $37,800.

The journal entry to close the overapplied overhead cost is attached in the image below.

What is underapplied or overapplied overhead cost for the year?

- Underapplied overhead is a circumstance in which overhead costs exceed the amount that a business really budgets for in order to operate.

- On a company's balance sheet, unapplied overhead is often shown as a deferred item that is balanced by adding a debit to the cost of goods sold (COGS) section before the end of the year.

- The direct expenses incurred during the manufacture of the products a business sells are known as costs of goods sold. An unfavorable variance is the amount of underapplied overhead.

- Underapplied overhead is when a company's real overhead costs exceed its budgeted costs. On a company's balance sheet, this amount is shown as a prepaid expense or short-term asset as a debit, which is subsequently balanced out by a credit for prepaid expenses and a debit for cost of products sold before the end of the fiscal year.

- A negative variance results from underapplied overhead when a company exceeds its budget. Because analysts and managers seek for trends that might indicate changes in the business environment or economic cycle, it is often not viewed negatively.

Calculate the company's predetermined overhead rate as follows:

Predetermined overhead rate =

= Machine hours

Machine hours

= $8 Per machine hour

Therefore, predetermined overhead rate is $8 per machine hour.

The graphic below shows how the T-account for manufacturing overhead is set up:

The whole amount of applied overhead is $187,200, whereas the total amount of incurred overhead is $225,000.

The sum of $37,800 is the underapplied overhead, which the corporation must increase in order to comply with the criteria as the actual overhead is higher than the applied overhead.

To learn more about underapplied or overapplied overhead cost for the year,

brainly.com/question/13981818

#SPJ4