Answer:

A.

Explanation:

In business, the term positioning is defined as a position where items or products stand in comparison with other products and services in the market.

External positioning refers to placing the price of services and items by taking cues from other similar products and services in the marketplace.

In the given case, the two companies are engaging in external positioning. Therefore, option A is correct.

Answer:

c. Strategic planning

Explanation:

Micromanaging things refers to managing things with respect to the subordinates work or remember them for working in a particular subject.

In the given situation, since Heidi Ganahl spent a lot of time for micromanaging things after that he spent more focused on strategic planning as she wants to do the work planning so that she is able to accomplish the goals and objectives in an efficient and effective manner

Moreover, strategic planning refers to planning with respect to the direction of the business, its vision, mission, objectives, goals, etc so that the firm gets to know where they are and where they want to be in near future.

Hence, the correct option is c.

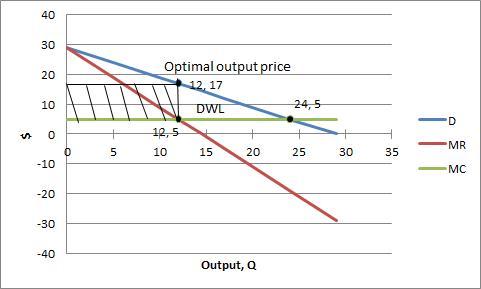

Answer:

a. Marginal Revenue = 5

b. Maximum profit = $144

c. Q optimum = 12 ; P optimum = $17

d. Social cost = $72

Explanation:

Step 1. Given information.

Step 2. Formulas needed to solve the exercise.

- Total Revenue=TR=P*Q=(29-Q)*Q=29Q-Q2

- Marginal Revenue=dTR/dQ=29-2Q

Step 3. Calculation.

Set MR=MC for profit maximization

29-2Q=5

2Q=29-5

Q=12 -----profit maximizing output

P=29-Q=29-12=$17 -------profit maximizing price

Total Profit=(P-AC)*Q=(17-5)*12=$144 ------Maximum Profit

Lerner's Index=(P-MC)/P=(17-5)/17=0.7059

<h2>

</h2><h2>

TAKE A LOOK TO THE ATTACHED IMAGE</h2>

Profit is shown by rectangular shaded area.

Socially optimal price P=MC=$5 --------Socially optimal price

We know P=29-Q, Set P=5

5=29-Q

Q=24 ---------Socially optimal output

Social Cost is equal to dead weight loss. It is shown by triangular area DWL

Social Cost=1/2*(17-5)*(24-12) =$72

Answer: Legitimate power

Explanation:

The source of power that Sherry has in enforcing Ollie's holiday scheduling policy is refered to as the legitimate power.

Legitimate power simply means the power that one has based on the formal position that is being held by the person in an organization. This usually applies to person who are in position of authority in the organization.

Therefore, the correct answer is legitimate power.