Answer:

$8,400

Explanation:

total commission = $300,000 x 8% = $24,000

50% co-brokerage split = $24,000 x 50% = $12,000

Walt's commission = $12,000 x 70% = $8,400

the 70% commission split between Walt and his broker means that Walt keeps 70% of the commission and the broker keeps 30%.

total commission is split between the two firms because the Walt's listing was sold by another firm.

Answer:

The question is missing the direct and indirect costs, however I will let you know how to calculate.

The costs will be given total for material, labor and overheads, along with this data a ratio in the form of a percentage will also be given for example material used in preparation of fresh bakery goods.

The amount of material will be multiplied by the percentage of material used in preparation of fresh bakery goods, the result amount will be the cost incurred for material used for the preparation of fresh bakery goods.

Explanation:

The question is missing the direct and indirect costs, however I will let you know how to calculate.

The costs will be given total for material, labor and overheads, along with this data a ratio in the form of a percentage will also be given for example material used in preparation of fresh bakery goods.

The amount of material will be multiplied by the percentage of material used in preparation of fresh bakery goods, the result amount will be the cost incurred for material used for the preparation of fresh bakery goods.

Follow this for all the cost heads provided.

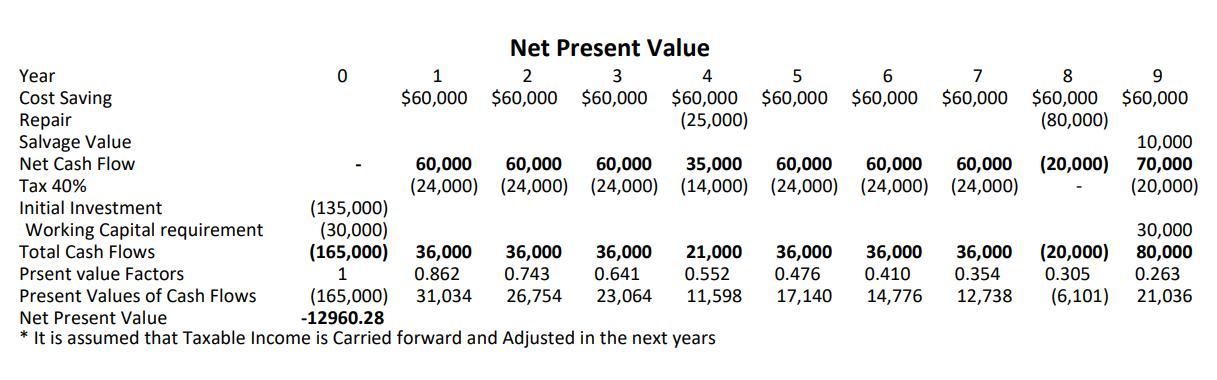

Answer:

NPV is -$12,960

Explanation:

Net present value is the Net value all cash inflows and outflows in present value term. All the cash flows are discounted using a required rate of return.

In this question all the expenses are cash outflows and The cost saving is the cash inflow from the new machine investment.

Working for the NPV is attached with the answer please find it.

Answer:

Option d is correct.

<u>Adapting to mergers</u>

Explanation:

The change agent has the activity close by to ingrain trust in the workforce by coming up unmistakably on the organisation's approach for the current workforce ( of past organisation) so they can make certain about their future with the organisation and decide their future strategy. Adapting to mergers is the correct choice as the change specialist needs to prepare the workforce work and submitted as ahead of schedule as could reasonably be expected.