Answer:

B) systematic risk

Explanation:

Federal Reserve changes in monetary policies affect the entire securities market hence considered a Systematic risk. It is also known as the Non-diversifiable risk ; it cannot be diversified away unlike stock specific or industry specific risk(unsystematic ) which can be eliminated through diversification.

Systematic risk is unavoidable and may be difficult to predict. Other examples include increase in long term interest rates, recessions or wars. Additionally, Investors are only compensated for systematic risk and not for diversifiable risk.

Is a Google Adwords Fundamental exam answer.

The correcta answer is:

determine if campaigns are meeting overall marketing and conversion goals

Explanation and more info:

http://www.certificationanswers.com/en/by-monitoring-ad-campaign-performance-an-advertiser-may-obtai....

Answer and Explanation:

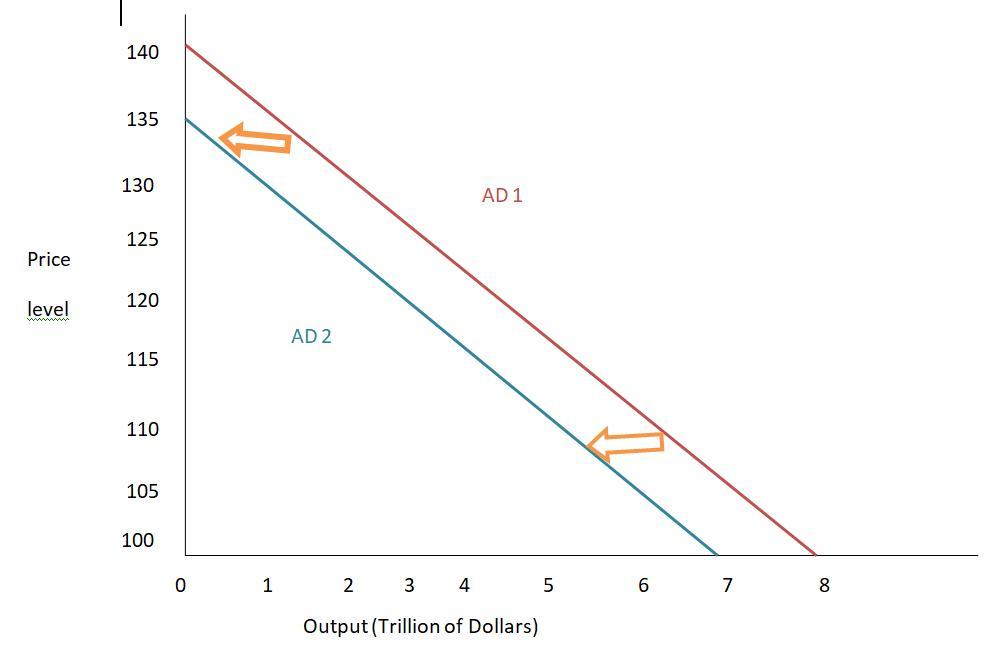

According to the scenario, computation of the given data are as follow:-

1) Marginal propensity to consume (MPC) for this economy is 0.75 as it denotes the spending of the household and saving of 0.25 and the spending multiplier for this economy is

= Spending Multiplier(M)

= 1 ÷ 1 - MPC

= 1 ÷ 1-0.75

= 1 ÷ 0.25

= 4

2). Decrease in government purchases will lead to a decrease in income, generating an initial change in consumption

= -Amount of Government Decrease Purchases by × MPC

= -$250 billion × 0.75

= -$187.5 billion

3). Decrease income again, causing a second change in consumption

= Amount Decrease in Government Purchases × MPC

= -$187.5 billion × 0.75

= $140.6 billion

4).Total change in demand resulting from the initial change in government spending

= Amount of Government Decrease Purchases by × Spending Multiplier(M)

= $250 × 4

= $1,000 billion

= $1 trillion

As we can see that the income falls by $1000 billion in the end, so AD shifts to the left by the size of $1 trillion

In the question the graph is missing. Kindly find the attachment for both of question and answer

Answer: B. reduces reported net income of the period but does not involve an outflow of cash for that period.

Explanation:

Depreciation is the wear and tear of an asset due to the use of the asset. When an asset is depreciated, such an asset is eventually sold at a scrap value.

The statement of cash flows (indirect method) reports depreciation expense as an addition to net income because depreciation reduces reported net income of the period but does not involve an outflow of cash for that period.

Answer:

TIE = 150,000 / 5,000 = 30

Explanation:

Times Interest Earned (TIE) = Earnings Before Interest and Tax (EBIT) / Interest Expense

TIE ratio shows the ability of a company to meet its interest payments on its debt (solvency), expressed in times.

In this case 3.33% of the operating profits goes towards servicing the debt or the operating income are 30 times the annual interest expense.